My name is Patricia Wills. I am a retired legal secretary of twenty-eight years — and when my daughter removed me from the family mailing list and started managing my affairs without asking, I sent a single certified letter that changed everything.

My name is Patricia Wills. I am a retired legal secretary of twenty-eight years — and when my daughter removed me from the family mailing list and started managing my affairs without asking, I sent a single certified letter that changed everything.

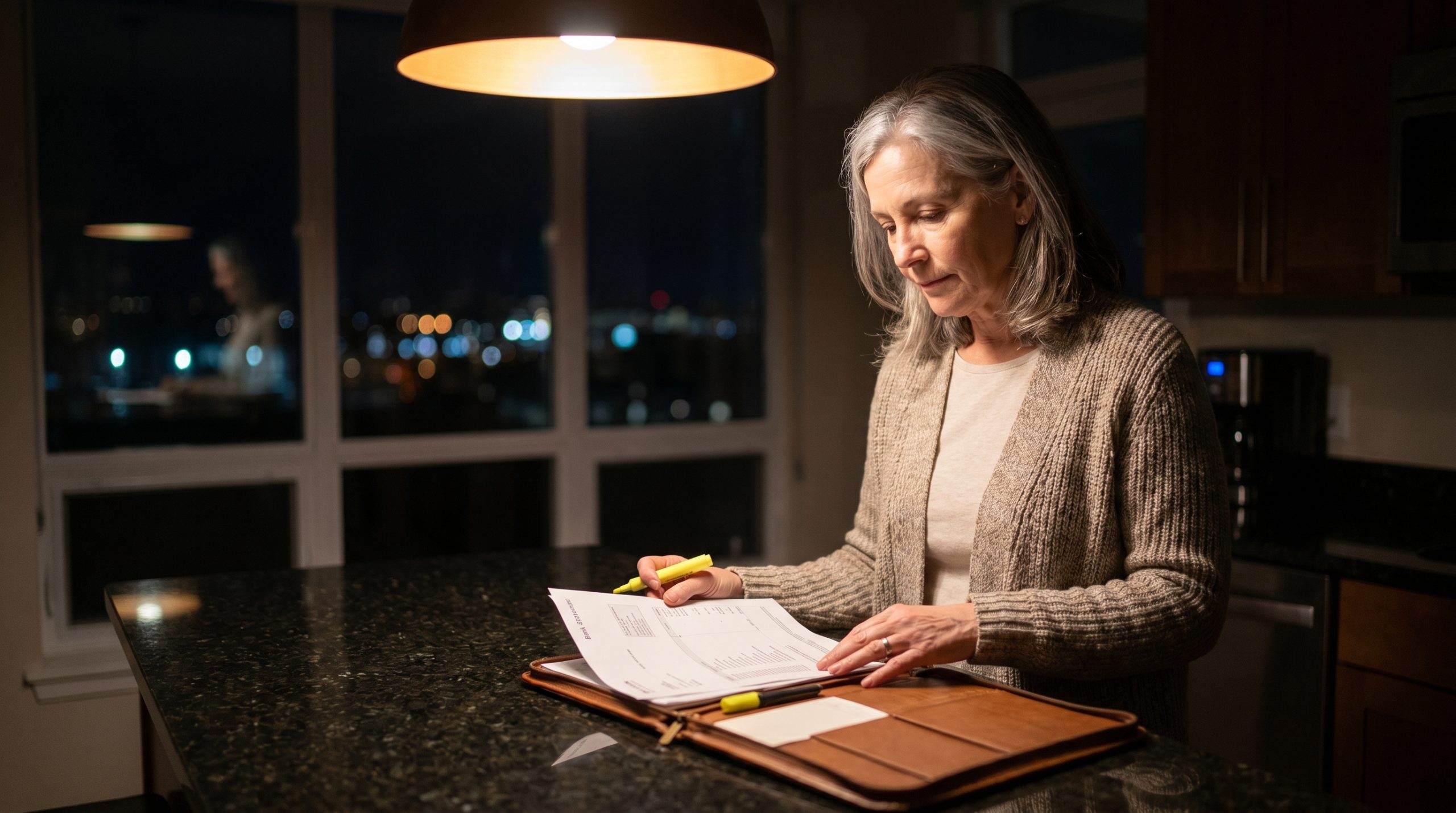

I opened the portfolio because I had not looked at the HELOC statement in two months.

It was Sunday evening, the night after Thanksgiving.

9:18pm by the clock on the stove.

The kitchen island was clear except for the leather portfolio, which had been sitting on the corner where I always kept it, and my coffee cup, which I set down beside it.

The overhead light was on.

The house was quiet.

Next door — two houses down, through the open window — I could hear the Tisdale kids laughing.

That would be Wallace and Tamra’s house.

They had driven up Wednesday evening for the holiday and were leaving in the morning.

I unclipped the HELOC statement from the portfolio.

TD Bank.

Home equity line of credit.

Primary borrower: Sylvia A. Tisdale.

Current balance: $32,000 drawn.

Credit limit: $80,000.

I set the statement down on the island.

I looked at the balance line again.

The last time I had looked at this account, in September, the balance had been $12,000.

The time before that — June — it had been zero.

I had not written a check against this line since I used it to replace the water heater in 2022.

I stood at the island for a moment without moving.

Then I picked up my phone to open the TD Bank app, and the family group text notification was still on the screen from eight minutes ago.

I had looked at it in the living room and come in here to think.

I had not replied.

I opened the thread.

The holiday-card design for the year was pinned at the top of the chat.

Tamra had sent it that afternoon — a photograph of her and Wallace and the kids, a clean white border, the Tisdale name in a script font I did not recognize.

Beneath it, she had posted a PDF attachment: “2025 Mailing List — Final.”

I had opened the PDF, scrolled through forty-seven addresses, and not found my own.

I had typed: “I’m not on the list?”

Tamra had replied at 8:46pm.

“Sylvia, we trimmed the list this year for administrative simplification. You’re at the house enough that the card is redundant for you. We’re doing what’s best for everyone. 🙂”

Wallace had not replied to the thread.

I put the phone face-down on the island beside the statement.

I have spent twenty-seven years as a commercial loan officer at a regional bank, the last eleven of which I spent as a senior credit analyst specializing in middle-market real-estate lending.

I personally underwrote eight hundred HELOC originations across those years.

My name is still on the bank’s internal HELOC origination checklist — the 2019 revision, which was never reissued because the process did not change again before I retired.

I know the forms, the authorization structures, the draw mechanics, and the revocation procedures for blank-check HELOC signers.

I know them the way a surgeon knows the instruments on the tray.

Not from studying them.

From using them, for two and a half decades, under real consequences.

In 2018, when I set up this HELOC, I added Tamra as an authorized signer with blank-check draw rights.

Not a co-borrower.

Those are different things.

A co-borrower shares legal liability and has equity authority.

An authorized signer has administrative authority — they can write checks against the line on the primary borrower’s behalf, for purposes the primary borrower has designated.

The distinction is in the addendum.

It is in writing.

I drafted the addendum.

I know what it says.

I had added Tamra because my house had flooded in 2018 — a kitchen pipe, while I was on a credit-union audit trip — and Wallace had needed someone with check-writing authority to pay the contractor.

Tamra was efficient and organized.

I trusted her to write one check.

I did not revoke the authorization afterward.

This was my error.

I have made two or three errors of consequence in my professional life.

I recognize them when I see them.

I looked at the HELOC statement.

The balance was $32,000.

I had not drawn $32,000.

I had not drawn anything since the water heater in 2022.

I picked up the statement and turned it to the transaction section.

The draws went back fourteen months.

September 2024 — $3,200.

October 2024 — $2,800.

November 2024 — $2,500.

I counted.

Fourteen draws.

Fourteen months.

$32,000 total.

I set the statement back on the island.

I did not feel anything in particular.

This is not a clinical achievement.

It is simply what it is like to recognize a known pattern.

I have reviewed two hundred and forty loan files where a draw history told a story the borrower did not intend to tell.

I know what a systematic draw pattern looks like.

I know how to read it.

I closed the portfolio.

I pressed one hand flat on the cover.

The leather was warm from the kitchen light.

The statement was beneath the cover, its edge visible at the bottom of the clip.

From two houses down, through the window, the kids were still laughing.

I could not hear Wallace.

I could not hear Tamra.

The only sound from that direction was the children, and the sound of a screen door, and then quiet.

I picked up my phone.

I did not open the family group text.

I opened the TD Bank app and navigated to the HELOC account.

I went to the transaction history.

I downloaded the full fourteen-month draw schedule as a PDF.

I saved it to the folder I keep for the house accounts.

I looked at the timestamp on each draw.

Each draw had a corresponding ACH outbound notation — mobile check deposit, cross-bank transfer.

I know what that means.

I know exactly what bank that money went to.

I had seen the Marcus by Goldman Sachs account in a linked-accounts view that Tamra had shared with me in 2018 and never revoked.

I had not looked at it in years.

I looked at it now.

The deposits matched.

Every draw from my HELOC had a corresponding deposit into Tamra’s sole-name Marcus by Goldman Sachs savings account within forty-eight hours.

The amounts were identical.

The timing was consistent.

Fourteen cycles.

Thirty-two thousand dollars.

I set my phone face-up on the island and looked at it.

Then I set it face-down.

I walked to the window over the sink and looked out at the dark back yard.

A car moved past on the street.

The kitchen light reflected in the window glass.

I could see myself standing there — the kitchen behind me, the portfolio on the island, the statement underneath the leather cover.

I walked back to the island.

I opened the portfolio again.

I found the yellow pen I keep in the left pocket of the portfolio — the one I use for review marks when I am going through a client file.

I highlighted the cumulative balance line on the HELOC statement: $32,000.

I underlined the draw total once.

I set the pen down on the statement.

I stood at the island for thirty seconds.

Then I picked up my phone.

I did not open the family group text.

I did not call Wallace.

I found Lou Fenton’s number in my contacts.

I pressed call.

It went to voicemail after two rings.

“Lou, this is Sylvia Tisdale. I have a HELOC situation I need to route through your unit. Account number—”

I read the account number from the statement.

“—the draw history goes back fourteen months, totaling thirty-two thousand. The authorized signer is a non-co-borrower. I’ll have a fraud package on the portal by end of business Monday. I’d appreciate routing it through your unit.”

I ended the call.

The time was 9:24pm.

I set the phone face-down on the leather portfolio.

The portfolio was still warm.

I left the kitchen light on.

I went to bed.

I have been on the Tisdale family holiday-card list since 1992.

That was the year Wallace’s father, Gerald, started the tradition.

He was methodical about it.

He kept the mailing list in a binder in his home office — a three-ring binder with dividers, updated every September when the new phone book came out.

He would mail forty, sometimes fifty cards.

He addressed each envelope by hand.

He included a photograph.

The family photograph, always formal: Gerald and Sylvia, then Wallace as a child, then Wallace as a teenager, then Wallace at college graduation, then — from 2017 onward — Wallace and Tamra.

Gerald died in 2019.

I took over the mailing list that year.

I kept it in a simple spreadsheet.

Forty-seven addresses.

I had mailed the cards every December until 2021, when Tamra asked if she could take over the logistics because she had a Canva template she liked and a printer that did glossy finish.

I said yes.

I sent her the spreadsheet.

I was on it.

I know this because I checked.

Monday morning, after Lou’s call, I went into my email and found the spreadsheet I had sent Tamra in November 2021.

The file was still in my sent folder.

My address was in row 3, below Gerald’s sister and above our old neighbors from Reedy River Drive.

I had been on it in 2021.

I had been on it in 2022, 2023, and 2024, because the cards had arrived and I had set them on the mantelpiece the way I always did.

In 2025, I was not on it.

In the PDF footer, in eight-point type, it said: “List trimmed for administrative simplification — Tamra.”

This is what the exclusion cost, before the money:

Thirty-three years of unbroken presence on a list my late husband started.

Gerald’s handwriting on forty envelopes, for the last time, in 2018.

My address, in row 3, the way he had always organized things — family first, then friends, then neighbors.

Tamra removed me from row 3 of a list Gerald built.

She did it while the HELOC she had been drawing against for fourteen months was still open.

She called it administrative simplification.

I did not say any of this on Monday.

I noted it in the way I note the details that belong in a file rather than a conversation.

The money is easier to describe.

I underwrite loans.

I have underwritten eight hundred HELOC originations.

I know how to build a draw history.

In September 2024, Tamra had written a HELOC check for $14,200.

The memo line on the check image, pulled from the TD Bank portal, said: “Kitchen reno — Tanner Contracting.”

This was the kitchen renovation in Tamra and Wallace’s own house — the island they finished, the one Tamra had mentioned at the Thanksgiving table as if it were something they had saved up for.

They had not saved up for it.

They had used my credit line.

In February 2025, Tamra had written a check for $6,500.

The Cozi app entry — which Sylvia could see because she was still listed as a “consulting member” — logged this as: “Keisha car loan assist — Keisha is Tamra’s younger sister.”

Six thousand five hundred dollars from Sylvia’s HELOC, for Tamra’s sister’s car down payment.

In June 2025, a check for $3,400.

The Cozi entry: “HH rental — July 4 trip.”

Hilton Head.

The July 4 trip that Tamra had mentioned in a group text as a “family investment in summer memory-making.”

Sylvia had not been invited.

The remaining $7,900 had moved in twelve smaller draws — ranging from $200 to $1,100 — over the fourteen months, deposited directly to the Marcus by Goldman Sachs savings account with no Cozi notation.

Rolling.

Gradual.

The kind of draw pattern that reads as noise if you are not looking at it as a series.

I was looking at it as a series.

I sat in my home office Monday morning with the HELOC statement, the Cozi export, and the Marcus linked-accounts view open on three browser tabs.

The leather portfolio was open on the desk beside me.

I had printed the fourteen-month draw schedule on legal-size paper.

I had clipped each draw entry to its corresponding Cozi notation.

Where there was no Cozi notation, I had written, in pencil beside the entry: “No documented purpose — rolling deposit, Marcus GS.”

The total was $32,000.

It was not a round number that invited a convenient explanation.

Thirty-two thousand dollars across fourteen months was a draw-and-deposit pattern.

Anyone who has reviewed two hundred and forty loan files knows what a draw-and-deposit pattern looks like.

I know what it looks like because I reviewed two hundred and forty loan files.

I am aware that Tamra did not think I would look.

She had been on the HELOC since 2018.

I had not looked at the billing tab in seven years except for the routine quarterly review I ran in September.

She had counted on the quarterly review producing a familiar $0 balance, the way it always had.

It had not.

I do not know whether she understood what an authorized signer is, as distinct from a co-borrower.

She had told Wallace, over the years, that she was “on the line” as if she had property authority.

She does not.

I drafted the 2018 addendum.

I know what it says.

I did not call Tamra on Monday.

I did not call Wallace.

The day before — at the Thanksgiving table — Tamra had said, “We should really talk about the kitchen, Sylvia. It came out so well. Tanner Contracting, if you ever need them. Reasonable prices, great finish.”

Wallace had refilled his glass.

The kids had been arguing about something at the other end of the table.

I had said, “It looks nice.”

Tamra had said, “It really does.”

She had picked up her fork.

She had moved on.

She had said it in the tone of a person passing along useful information.

The tone of someone who believed she had done something ordinary.

The kitchen renovation that Tanner Contracting had completed.

Fourteen thousand two hundred dollars.

From my credit line.

On my house, secured against my property.

I thought about the Thanksgiving table.

I thought about the way Tamra had said “Tanner Contracting, if you ever need them” — the casual, neighborly quality of the recommendation, as if she were sharing a contractor who had done work for her own money.

I thought about this for approximately ninety seconds.

Then I stopped thinking about it.

I sat at the desk in the morning light and I thought about Gerald’s binder.

The three-ring binder with the dividers.

The way he addressed the envelopes by hand, because he said a machine-printed label on a Christmas card missed the point.

The forty-seven addresses.

My address, in row 3.

I had not thought about Gerald’s binder in several years.

I thought about it now for about four minutes.

I thought about the fact that Tamra had removed me from a list Gerald started in the same administrative gesture that she used to log a $6,500 car payment for her sister as a family expense.

I thought about row 3.

I did not say these things to anyone.

They were not things to say to anyone.

They were things to know.

Then I closed the Marcus linked-accounts browser tab.

I pulled up the TD Bank secure-mail portal.

I began assembling the fraud package.

The fraud package is a standard TD Bank internal format — thirty-two pages, one draw cycle per page.

Each page contains: the check image from the HELOC, the corresponding Marcus deposit confirmation pulled from the linked-accounts view, and a one-line annotation matching the draw amount to the documented or undocumented purpose.

I know this format because I trained junior loan officers in it for a decade.

I know the routing, the case numbering, the escalation path.

I know the name of the regional special-investigations manager who will receive the file.

I trained him twelve years ago.

At 7:14am, Lou Fenton had returned my voicemail.

He was careful and explicit.

“Sylvia, submit the package on the secure-mail portal under my case number. I’ll have the line frozen by end of business and the revocation logged. You don’t need to call them again — I’ll route it from here.”

He paused.

“I owe you a thousand favors. Use this one.”

I had written the case number on the HELOC statement in the top right corner.

Below the case number I had written the Form HE-22-RVK number — the blank-check authorization revocation form.

I did not feel vindicated.

I did not feel anything in particular that I would name.

I felt the weight of a file that was complete and correct and needed to be submitted.

I had felt this before, many times, sitting at a desk with a loan file that was complete and needed to go to underwriting.

The file was always just a file.

What mattered was whether the work inside it was accurate.

This one was accurate.

That is all the feeling I had, and it was enough.

The fraud package took four hours to build.

I have submitted three internal fraud packages in my professional life, all as the reviewing officer on behalf of a borrower, and I know the format.

One page per draw cycle.

Each page: the check image from the HELOC, the corresponding deposit confirmation from the receiving account, and a one-line annotation matching the draw to a documented or undocumented purpose.

The check images came from the TD Bank portal, downloadable under primary-borrower authority.

I downloaded all fourteen.

The deposit confirmations came from the Marcus by Goldman Sachs linked-accounts view — the joint access Tamra had set up in 2018, when I had briefly linked our accounts for the contractor emergency, and never revoked.

She had forgotten the view existed.

I had not.

I had not used it in years.

I used it now.

I pulled fourteen deposit records.

Each matched a HELOC draw within forty-eight hours.

The ACH timestamps were exact.

The Cozi annotations came from the export I had run the night before.

Cozi keeps revision history on budget entries.

Tamra had logged most of the draws under her own “house renovation” and “family expenses” categories, which meant she had documented their purpose herself.

I matched twelve of the fourteen draws to Cozi entries.

The remaining two — $1,100 and $900 — had no Cozi entry.

I annotated those: “No documented purpose — rolling deposit, Marcus GS — ACH trace confirms cross-bank transfer within 48h of draw.”

I printed the package.

Thirty-two pages.

I went through each page once with a red pen, confirming the amount match.

Every draw matched.

Every deposit matched.

The timing across all fourteen cycles was within forty-eight hours.

I clipped the thirty-two pages with a binder clip and set them on the desk.

I prepared a one-page cover sheet: account number, primary borrower name, authorized signer name, revocation basis, case number, submitting officer, date.

I attached the cover sheet to the front.

This was not the Precision Decision.

This was preparation.

The fraud package being complete did not mean the revocation was filed.

It meant I had the instrument.

At 11:02am, I logged into the TD Bank secure-mail portal.

I uploaded the thirty-two-page fraud package under Lou’s case number.

The upload confirmed at 11:08am.

At 11:14am I submitted Form HE-22-RVK — the blank-check authorization revocation form — electronically through the same portal.

“Revoke the authorization. Submit the package. Close the line.”

That was what I had said to myself, standing at the kitchen island the night before.

Nine words.

The revocation confirmation arrived at 11:16am.

I looked at the confirmation email.

I did not celebrate.

I filed the email in the “HELOC — 2025” folder.

At 11:32am, Tamra sent a message to the family group text.

A photograph of the new kitchen pendant lights they had installed over the island.

“Final touch — in time for Christmas! Tanner really nailed the finish. 🎄”

No mention of the payment source.

No mention of the certified-mail letters that had not yet been drafted.

She did not know.

The check she had been planning to write — $1,800, for a landscaping invoice from a contractor named Del Vásquez — had not yet been returned.

I looked at the photograph of the pendant lights.

They were attractive — a brushed brass finish, two of them over the kitchen island, on a dimmer switch by the look of the hardware.

I closed the group text.

I drafted the certified letters at 12:15pm.

Two letters, identical.

One addressed to Tamra Tisdale at the home address on the HELOC addendum.

One addressed to Wallace Tisdale at the same address.

Each letter was one page.

Each stated: the blank-check draw authorization held by Tamra Tisdale has been revoked, effective 11:16am Monday; the HELOC is frozen pending special-investigations review; a fraud package has been submitted to TD Bank’s special-investigations unit under case number [Lou’s case number]; the primary borrower remains the owner of the underlying credit line and the sole authorized party to any future draws.

I did not use the word “theft.”

That is not the word the bank form uses, and I do not use words that are not in the form.

The bank has its own language for what happened.

I used the bank’s language.

I drove to the post office at 4:15pm.

I mailed both letters certified.

I kept the tracking receipts.

I came home.

I made coffee.

I sat at the kitchen island.

The leather portfolio was closed.

I had set it at the side of the island, the way I always do when a file is complete — off the working surface, to the side.

The cover was still warm from where I had set my palm on it the night before.

I put my hand on it again.

It was cool now.

I had a thought about the holiday-card list.

Not about Tamra’s name on it, or my absence from it.

About Gerald’s handwriting on the envelopes.

He had addressed them with a fountain pen — a blue-black ink — and he wrote in the style of a man who had learned penmanship in grade school and never stopped using it.

My name and address, in his handwriting, every December until 2018.

It had not occurred to me, while he was alive, to think of the envelopes as a record of something.

It occurred to me now.

I did not decide anything based on this.

I drank my coffee.

The kitchen was quiet.

Outside, the November light was going low and orange behind the neighbors’ roof line.

The pendant lights in Wallace and Tamra’s house two doors down would be on by now, bright over their new island, the brushed brass reflecting off the quartz.

I had seen the photograph.

They were attractive lights.

I waited for Tuesday.

The certified letters would be delivered Tuesday.

The check Tamra had written for the landscaping invoice would be returned Tuesday.

She would find out the way the bank always intended people to find out — not from a phone call, not from a warning, but from the instrument itself telling her that the instrument was gone.

That was the correct order.

I had not invented it.

I had taught it to junior officers for a decade.

It was simply how it worked.

Tamra found out Tuesday morning.

The landscaper — a man named Del Vásquez, who had laid the new stone walk at the side of Tamra and Wallace’s house — called Tamra at 10:47am.

The $1,800 check she had given him the week before had been returned.

He needed another form of payment.

He was polite about it.

He mentioned it might be a bank error.

Tamra logged into the TD Bank HELOC online view at 11:14am.

The screen showed: “Account frozen pending special-investigations review.”

Below that, under signer status: “Tamra Tisdale — authorization revoked, 11:16am Monday.”

She called Wallace at 11:20am.

Wallace had opened his certified letter that morning when the mail arrived.

He read it.

Then he called me.

“Mom, what is this?”

“It is what it says,” I said.

“Tamra is —” he stopped. “She says there’s been a misunderstanding. She wants to explain.”

“You both may come to the house Wednesday at six o’clock.”

Wallace paused.

“Can you just — can you call her? Can you just talk to her first?”

“Wednesday at six,” I said.

I hung up.

Wallace and Tamra arrived at 5:48pm Wednesday.

They had come from their own house, twelve minutes away.

Wallace’s car was in the driveway.

I had left the porch light on.

I opened the door and let them in.

I did not offer them coffee.

We sat in the living room.

Tamra sat on the end of the sofa closest to the fireplace.

Wallace sat beside her.

I sat in the chair across from them — the same chair I have sat in for thirty years, the high-backed one with the read arm that Gerald used to comment on because he thought it made the room look like a law office.

The leather portfolio was on the side table next to me.

I did not open it.

Tamra spoke first.

“Sylvia, this is a misunderstanding. The kitchen was for our whole family — we all use that house when we visit. The line was always meant for shared expenses. You added me to that account because we’re family. We didn’t think it needed to be a formal process every time.”

She held my gaze.

Her hands were folded in her lap — the same posture as the family meeting at the hospice, in another story, in another woman’s kitchen.

These things repeat.

I said nothing.

I looked at her.

She continued.

“The kitchen is something everyone benefits from. When the kids visit. When Wallace and I host. You’ve seen it — it came out beautifully. I thought that’s what the line was for. I genuinely believed that.”

Wallace was looking at his hands.

I said: “The 2018 addendum named you as an authorized signer. Not a co-borrower. Those are different things.”

“We didn’t go over the legal language in —”

“I know what the addendum says. I drafted it.”

She was quiet for a moment.

Then she shifted.

“Sylvia, I hear that you’re upset. I should have talked to you before I used the line for the kitchen. I see that now. And the card thing —” she paused, “— I should have asked. I didn’t know you’d feel that way about the mailing list. Let me put you back on it tonight. I’ll call Canva. We can reprint. The cards haven’t gone out yet.”

She leaned forward slightly.

“You’re at the house enough that I didn’t think — I should have asked. You’ve been isolated since Gerald. I worry about you. I think you’ve been alone with this for a long time and it’s made things feel bigger than they are. Let me sit with you for a bit after Wallace leaves.”

Wallace looked up.

His expression said: please let this be over.

I did not say anything for four seconds.

I looked at the leather portfolio on the side table.

Then Tamra’s voice changed.

“This is what you do, isn’t it.”

Not a question.

“You collect things. You wait. And then you ambush. Wallace told me what you did to his sister fifteen years ago — how you waited until the right moment and then took everything away from her. You’re not protecting yourself. You’re punishing me for being in this family. For making Wallace happy when you couldn’t.”

Her voice was controlled.

She was not shouting.

She was making a careful argument in the tone of someone who had prepared it.

Wallace said, “Tamra —”

She held up one hand.

I waited until she had finished.

Then I said: “The 2018 addendum named you as an authorized signer. The signer authority is revoked. The line is frozen. The fraud package will resolve under bank procedure. I want you to leave the house by seven-thirty. Wallace, you may stay if you choose.”

Tamra looked at me.

She looked at the portfolio on the table.

She looked at Wallace.

Wallace was looking at his shoes.

She stood.

She picked up her bag from the sofa cushion.

She walked to the door.

Wallace stood.

He followed her, half a step behind, the way he had been following her, I thought, for several years.

I did not stand up.

I let them see themselves out.

The door closed at 7:18pm.

I sat in the chair.

The room was quiet.

The fire was not lit — it was November but not cold enough for a fire, and I had not thought to light it.

The porch light was still on outside.

I could see it through the window, a pale yellow oval on the front step.

I picked up the leather portfolio from the side table.

I held it in my lap.

I thought about what Tamra had said about Wallace’s sister.

The story she had told him, or the version of it she had been told, or the version Wallace remembered, at fifteen, when he had not yet been old enough to understand what the situation had actually been.

I had made the right decision then also.

That was what I had.

Right decisions, correctly made, imperfectly received.

I set the portfolio back on the side table.

I went to the kitchen and turned off the overhead light, the one that had been on when I found the HELOC statement on Sunday.

The kitchen was dark.

I went to bed.

The special-investigations review resolved in eleven weeks.

TD Bank recovered $24,400 from Tamra’s Marcus by Goldman Sachs deposits — the draws that were within the look-back window.

The remaining $7,600 became my primary-borrower obligation.

I paid it from my savings.

I then closed the HELOC entirely.

I have not spoken to Tamra since the Wednesday-evening meeting.

I have not received the holiday card.

I did not expect to.

Eleven days after the Wednesday meeting, on a Saturday morning, Wallace drove to my house alone.

He did not call first.

He parked in the street.

He came up the front walk carrying a paper bag from the bagel place on Stone Avenue.

He rang the doorbell.

I opened the door.

He was in his weekend clothes — the gray Patagonia he has worn since 2018, the one Tamra says is too old to wear in public.

He was holding the paper bag with both hands.

I let him in.

He sat at the kitchen island.

He put the paper bag on the island and set his keys beside it.

He looked at the island surface for a moment.

“I read the 2018 addendum yesterday,” he said. “I went to the credit union and got a copy. I didn’t know what it said.”

“I know you didn’t,” I said.

He was quiet.

He looked at the paper bag.

He opened it and took out a sesame bagel and put it on the counter in front of him.

He did not eat it immediately.

“Mom —”

“You don’t have to,” I said.

He looked up.

I said: “Come by Saturday next week if you want to. Call first.”

He nodded.

He picked up the bagel.

He ate it.

He asked where I kept the good coffee now.

I pointed to the cabinet above the toaster.

He made a pot.

He stayed for forty minutes.

He did not mention Tamra’s name.

I did not mention the holiday card.

We talked about his practice — he has taken on three new patients, one of them a high school cross-country runner with a recurring IT band issue, and he has been trying a new protocol.

He described it.

I asked a few questions.

He answered them.

At the end of forty minutes he stood up, rinsed his coffee cup, and set it beside the sink.

He did not say it was okay.

I did not tell him that I forgave anything.

He nodded at me at the door.

He drove home.

I did not invite him to stay for lunch.

I accepted the bagels.

The second one I ate standing at the island at noon, with a cup of the coffee he had made, which was slightly too strong but not unreasonably so.

The kitchen was quiet.

Outside, the December light was flat and gray and adequate.

The apartment is four miles from the old house.

I moved in February.

The house sold in January — closing on the fourteenth, a Tuesday — and the equity went to pay down the HELOC balance and fund the deposit here.

The old house had been mine since 1988.

Gerald and I had bought it from a couple named Tillman who were moving to Charlotte for work.

I had the kitchen counter replaced in 1994.

I replaced the water heater in 2022 with the last draw I ever took against the HELOC.

The house sold in January for a price that would have seemed impossible to Gerald in 1988 and that seemed exactly right to me in January 2026.

I signed the papers.

I moved.

The apartment has two bedrooms.

I use the second bedroom as an office.

The leather portfolio is on the second shelf of the small bookcase I brought from the old house.

It is standing upright, clasp pressed shut.

I do not open it.

The HELOC closed in February, one week before the move.

The fraud package resolved three weeks after that.

The portfolio is the closed record of a concluded file.

There is nothing in it that needs revisiting.

On the kitchen table — a smaller table than the island, round, with two chairs — there is a new manila folder.

The tab reads: “Greenville Housing Trust — Q1 advisory consult.”

I am doing part-time advisory work with a small CDFI that helps first-time homebuyers navigate the pre-approval process.

The work is three mornings a week.

I sit across from people who do not yet understand what an escrow waiver is, or why the interest rate on a HELOC is variable, or what it means to be the primary borrower on a line of credit as distinct from an authorized signer.

I explain these things in plain English.

I have spent twenty-seven years learning to explain them in plain English.

The work is not complicated.

It is simply useful.

Tuesday, 10:15am.

Marisol Cisneros sits across from me at the kitchen table with her pre-approval documents.

She is thirty-three.

She works as a school nurse at Chandler Elementary.

She has saved enough for a five-percent down payment on a two-bedroom in the North Main corridor.

She wants a porch.

She is specific about the porch.

The apartment kitchen window faces east.

The morning light is coming straight in.

The window is open.

The bakery one floor down — Remy’s, sourdough, open since six — sends a smell up through the ventilation that I have come to associate with Tuesday mornings the way I used to associate the kitchen overhead light with Sunday evenings.

The two of us fit comfortably at the table.

There is room for the documents and two coffee cups.

Marisol asks what an escrow waiver actually means.

I tell her.

I tell her in the same way I told two hundred and forty loan applicants over twenty-seven years — not simplifying it into uselessness, not overcomplicating it into anxiety.

The middle register.

She nods.

She writes something in the margin of her document.

She asks about the HELOC line item on her homebuyer packet — the part that describes what a home equity line is and whether she should open one after purchase.

I tell her she should understand what she would be signing before she signed it.

I tell her that the addendum language matters.

I tell her that the distinction between a co-borrower and an authorized signer is not obvious but it is important.

She asks why.

I tell her, in practical terms, without reference to my own situation.

She writes more margin notes.

We work through the rest of the packet together.

It takes fifty minutes.

Marisol closes her folder.

She stands.

She says, “Same time next Tuesday?”

I say, “Same time.”

She picks up her bag.

I walk her to the door.

I return to the table.

The coffee cups are still there.

I rinse both of them in the sink.

I set them upside down on the towel beside the tap.

I look out the kitchen window.

The light has moved.

It is coming from higher up now, through the upper half of the window glass, and the sourdough smell has faded — Remy’s has moved on from the first bake of the morning.

The leather portfolio is on the bookcase shelf in the second bedroom.

Marisol does not know it is there.

There is no reason she would.

I dry my hands on the dish towel.

I pick up my pencil.

I open the Housing Trust folder.

I write Tuesday’s date at the top of a new page.

I begin the notes for next week’s session.

THE END.