My husband cancelled my long-term-care policy on the morning of my orthopedic surgery, and the policy declarations page in my desk drawer had every premium I had paid for nineteen years

The kitchen on Sweetbriar Lane was always cold on a Tuesday morning in October before the heater caught the back hall.

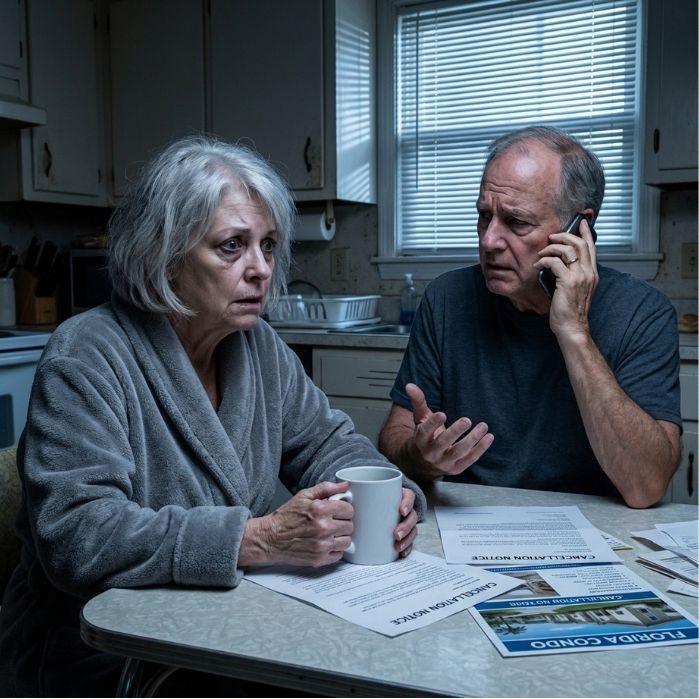

I sat at the kitchen table at six-forty in the morning in the same gray jersey robe I had worn since 2019 and the slippers my daughter had given me for Christmas in 2022.

The surgery was scheduled for ten-fifteen at the Mississippi Baptist Medical Center on North State Street.

It was a partial hip replacement on the right side.

The orthopedic surgeon was Dr. Renata Boyer.

I had been off solid food since midnight.

I had a small white cup of black coffee in front of me.

My husband Gary was at the other end of the table.

He was sixty-five years old and had been retired from his job as a warehouse manager at the McCardell distribution center on Highway 80 since the spring of 2023.

He had his own coffee in a white mug with the Allstate logo I had given him at a regional Christmas party in the early nineties.

He had been on his phone scrolling through a real-estate listing on the Gulf Coast he had been looking at for two years.

He set the phone face-down on the table.

He said, in the bright, cheerful tone he used when he was about to tell me a household decision he had already made, “Honey, I called Allstate and cancelled the LTC policy this morning. The cash value is going toward the Florida condo. We don’t need both. You’ll be fine after surgery — you always are.”

The kitchen was quiet.

The refrigerator hummed.

The clock above the stove made the small click it made at the top of every minute.

I held the coffee cup at the rim with two fingers.

I did not put the cup down.

I did not pick it up.

I held it where it was on the table.

My name is Marlene Whitfield.

I am sixty-two years old.

I worked as a property claims adjuster at the Allstate Mississippi regional office in Jackson for thirty-three years, from June of 1991 to my retirement on March 31, 2024.

I closed two thousand and ninety-six homeowner claims after twenty-one named tropical systems and four ice storms.

I walked the lots myself.

I trained eleven junior adjusters out of the Jackson office.

The commission plaque the company gave me at retirement hangs on the second-floor wall of the regional building on East Capitol Street.

In April of 2006, eighteen years and seven months before this Tuesday morning, I had walked into the broker office of an independent insurance agent on North State Street and opened a long-term-care policy for myself.

The premium was four hundred and seventy-eight dollars a month.

I paid it from a separate account at the BancorpSouth branch on Lakeland Drive that had only my name on it.

I paid that premium for nineteen years and four months.

I paid it through the year my mother died.

I paid it through the year my father died.

I paid it through the two years I supported my older brother’s wife after he passed in 2014.

I paid it through the months I covered our daughter’s tuition at Mississippi College in 2008 and 2009 because the housing scholarship had run out.

I paid it through the long Christmas in 2017 when Gary had been laid off for eleven weeks and I had covered the mortgage on Sweetbriar Lane out of the same account.

The policy was nineteen years old this April.

The cash value at the most recent annual statement, dated October 1, 2025, had been twenty-four thousand, three hundred and seven dollars.

Gary watched me hold the cup at the rim.

He said, “Mar. It’s the right call. You’re going to come through this surgery the way you came through the carpal tunnel and the kidney stone and the gallbladder. Your sister Charlene came through hers in 2019 and she didn’t need a policy either.”

He did not know that Charlene’s policy had paid out forty-one thousand dollars over fourteen months of in-home care.

He had not asked.

Gary’s brother Vince had been pushing the Florida condo plan for the better part of two years.

Vince was sixty-eight, divorced once, on his second marriage to a woman named Stacey from Hattiesburg.

Vince and Stacey had bought a unit in a complex in Destin in 2023 and had been calling Gary every Sunday afternoon to talk about the price-per-square-foot in the same complex.

Gary had been on the listing app for the same complex for fourteen months.

I set the coffee cup down on the table.

I did not set it down hard.

I set it down the way I set down a claim folder when a homeowner was waiting on the other side of the desk for me to tell them the deductible.

I said, “I have surgery in three hours, Gary.”

I said it once.

I did not say it twice.

Gary said, “Yes. And after the surgery we’ll talk about Destin. The deposit is already in. The closing’s in November.”

I said, “I’ll be ready at nine-fifteen.”

I picked up the cup.

I drank the coffee.

I rinsed the cup at the sink.

I put it on the rack to dry.

I walked through the hall to the small home office at the back of the house, the room that had once been our daughter’s bedroom and which I had taken over in March of 2024 when I had moved my files home from the regional office.

The office had a single window looking out on the small back yard.

It had my desk against the side wall, a metal four-drawer file cabinet on the right side of the desk, and the small bookcase that held my old field manuals.

On the desk by the laptop, where it had sat since the afternoon of my retirement luncheon, was the 1989 leather adjuster’s portfolio my supervisor Mr. Halverson had given me at the end of my first full year on the road.

The portfolio was dark brown calfskin.

The clasp was a small brass tongue that fit through a leather loop.

The lower right corner was monogrammed in gold leaf with the initials MW — for Marlene Whitfield, which had been my name at twenty-eight and was still my name at sixty-two.

The leather along the spine had darkened along the long edge where my right hand had carried it for thirty-three years.

I had carried that portfolio to two thousand and ninety-six homes.

I had carried it through Hurricane Katrina in 2005, when I had logged ninety-one storm claims out of the Hattiesburg field office in fourteen days.

I had carried it to the regional Christmas party in 2011, where my supervisor at the time had announced my promotion to senior adjuster in front of the regional manager.

I had carried it to my retirement luncheon in 2024.

It had sat on my desk every working day for the eighteen months since.

The bottom drawer of the file cabinet was locked.

The key was on a small split ring inside a coffee cup of pens at the corner of the desk.

I unlocked the drawer.

I lifted out the folder marked POLICIES — LTC — 2006 to PRESENT.

I set the folder on the desk beside the leather portfolio.

I opened the folder.

The top page was the most recent annual declarations page, dated April 14, 2025, from the same long-term-care carrier I had bought the policy with in 2006.

The declarations page showed the insured: Marlene W. Whitfield.

The owner: Marlene W. Whitfield.

The premium payor: Marlene W. Whitfield.

The premium: four hundred and seventy-eight dollars a month.

The benefit: a daily in-home care allowance of two hundred and fifty dollars and a facility allowance of three hundred and twenty-five dollars, for a maximum of forty-eight months.

The cash value as of the policy anniversary: twenty-four thousand, three hundred and seven dollars.

The signature line at the bottom of the declarations page said Marlene W. Whitfield.

It said it the same way my closing signatures on two thousand and ninety-six claim files had said it.

I had not signed any cancellation form.

I had not authorized any reassignment of cash value.

I had not had a single conversation with anyone at the carrier about closing the policy.

Gary did not have a power of attorney on the policy.

He had a power of attorney on a separate investment account I had opened in 2018, which I had signed for him because he had been the one to drive me to the broker’s office the week after my mother had been moved into the Madison memory unit and I had not slept for four nights.

The LTC policy and the investment account were not the same account.

They were not the same number.

They were not at the same institution.

They were not on the same letterhead.

The carrier kept its records in a regional office in Birmingham, Alabama.

The investment account was at a small firm called Pinebelt Capital, on Lakeland Drive, three blocks from the BancorpSouth branch where the premium account had been since 2006.

I lifted the folder.

I closed it.

I set it next to the leather portfolio on the desk.

I picked up the leather portfolio with both hands.

I held it.

The leather was the same weight in my hands as it had been the morning Mr. Halverson had given it to me in his office on the second floor in 1989.

I set the portfolio down beside the folder.

I sat down at the desk for a moment in the chair I had used for nineteen months.

I looked at the small window over the back yard.

The sun was up by then over the line of pines along the back fence.

The lawn had been mowed by the Sweetbriar HOA crew on Friday.

I touched the bottom-right corner of the portfolio with two fingers.

I did not open the portfolio.

I did not open the folder again.

I stood up.

I walked back through the hall to the bedroom.

I changed out of the robe into the loose track pants and the loose Mississippi State T-shirt the surgery prep sheet had told me to wear.

I packed the small overnight bag the prep sheet had told me to pack.

I came back down the hall at nine-twelve.

Gary drove me to the Mississippi Baptist Medical Center on North State Street.

He pulled up at the surgical-admissions door at nine-forty-seven.

He came inside with me to the registration desk.

He sat in the waiting area with his phone while I went back to pre-op.

I did not tell anyone in the pre-op bay about the LTC policy.

I signed the surgical consent in the same hand I had signed two thousand and ninety-six claim files.

The anesthesiologist started the line at ten-eleven.

I came out of recovery at twelve-forty.

I was wheeled to the orthopedic floor at one-fifteen.

Gary was in the chair by the window of the room.

He stood when the bed came in.

He said, “Mar. The doctor said you did great.”

I said, “We will not talk about the policy in this room.”

I closed my eyes.

The portfolio was on the desk in the back office at the house on Sweetbriar Lane.

The folder was beside it.

The cash value was sitting in a different account I did not have my name on.

The cancellation form had been faxed.

The signature on the cancellation form was in a file at the carrier’s regional office in Birmingham, Alabama.

I would see it in fourteen days.

I was discharged from Mississippi Baptist on the Friday afternoon at three-twenty.

Gary drove me home in the Sequoia.

I rode in the back so I could keep the right leg straight on the bench.

I went up the front walk on the aluminum walker the discharge nurse had set me up with.

I went to the small guest room on the first floor, the one we had set up for my mother in 2018 before we moved her to the Madison memory unit.

I lay down on the twin bed with the right leg elevated on the wedge pillow.

I closed the door.

Gary made a chicken-and-rice casserole that night.

He brought a plate in to me on a tray.

He set the tray on the bedside table.

He said, “Mar. The closing on the condo is the eighteenth. I’ll need you on the line for the title call. You don’t have to come down.”

I said, “Thank you for the casserole, Gary.”

He said, “Mar.”

I said, “Close the door.”

He closed the door.

I did not eat the casserole.

The recovery sheet said to walk a hundred feet, twice a day, beginning the day after discharge.

I walked the hundred feet on Saturday morning along the back hall.

I walked the hundred feet on Saturday afternoon along the back hall.

The home office was eleven feet from the door of the guest room.

The leather portfolio was on the desk.

The folder marked POLICIES — LTC — 2006 to PRESENT was beside the portfolio.

I sat at the desk in the chair from the dining room my daughter had brought in on Friday evening before she had driven back to her apartment in Memphis.

I sat in the chair for twenty minutes on Saturday morning.

I did not open the folder.

I did not open the portfolio.

I opened the laptop instead.

I logged into the BancorpSouth account on Lakeland Drive — my separate account.

The October premium of four hundred and seventy-eight dollars had been pulled on the second of the month, as it had been on the second of the month for two hundred and twenty-seven consecutive months.

The withdrawal had cleared.

I logged into the carrier’s policyholder portal on a tab I had bookmarked years ago.

The portal said: POLICY STATUS — CLOSED — CASH VALUE DISBURSED 10/14/2025.

The cash value of twenty-four thousand, three hundred and seven dollars had been disbursed by ACH to a bank routing number I did not recognize, into an account number that did not match any account I had ever held.

The closure had been initiated on October 9, 2025.

The surgery had been on October 14, 2025.

The threshold sentence at the kitchen table had been at six-forty in the morning of October 14, 2025.

Gary had told me five days after he had signed the paperwork.

I closed the laptop.

I sat at the desk in the dining-room chair.

I thought about 1992.

It was the only year I thought about for the first ten minutes.

I had been twenty-nine.

My mother had gone in for a hip surgery at the University of Mississippi Medical Center on a Tuesday in May.

The surgery had been routine.

The complication had come on the Friday — a pulmonary embolism that the floor team had not caught in time.

She had died on Saturday morning.

Gary had been twenty-eight.

He had driven me to the funeral home that Sunday afternoon.

He had sat with my mother’s minister, Pastor Royce, for an hour in the small office behind the chapel while I picked out the songs from the hymnal on Pastor Royce’s desk.

When the hymn list was done, Gary had walked me out to the parking lot.

He had said, in the doorway of the funeral home where the smell of the carpet cleaner had been the strongest, “Mar, I’ll handle whatever you need. You just sit.”

I had heard, that Sunday afternoon at the funeral home: My husband sees what is coming.

I had not asked him to repeat it for thirty-three years.

I had bought the long-term-care policy in April of 2006 because I had heard him say it once in 1992.

I had paid the four hundred and seventy-eight dollars a month from a separate account so that the policy would not be a household line item Gary had to think about.

I had thought, for nineteen years, that he had been quietly proud of it.

I sat at the desk on Saturday morning in October of 2025 and I understood, with the clarity of a thirty-three-year claim career, that the 1992 sentence and the 2006 policy and the 2025 cancellation were three different policies in three different file drawers.

I had filed them in the same drawer for thirty-three years.

That had been my filing error.

I picked up the phone at ten-fifteen on Saturday morning.

I called Pat Brewster.

Pat had been a property adjuster in the same Jackson office for twenty-one years before she had retired in 2022.

We had worked the same storm rotations from 2001 to 2022.

We had shared a desk in the field trailer in Hattiesburg after Katrina in 2005 for nine days straight.

We had not seen each other socially in eighteen months.

She picked up on the second ring.

She said, “Mar.”

I said, “Pat. I need an hour of your time today, in your living room, with no one else there.”

She said, “Come at eleven.”

I said, “I need a ride.”

She said, “I’ll be in your driveway at ten forty-five.”

I told Gary at ten thirty-five that Pat was coming to drive me to her house to drop off the book I had borrowed in March.

Gary said the casserole was in the fridge if I wanted it later.

He went out to the garage to clean the rims on the Sequoia.

Pat pulled into the driveway at ten forty-four.

She drove a 2019 Ford Edge in a dark blue.

She helped me into the front passenger seat with the walker folded behind.

We drove twelve minutes east to her house off Old Canton Road.

Pat’s living room had the same brown leather sofa she had bought from Mathis Furniture in 2007, two reading chairs, and a small oak coffee table.

I sat on the leather chair by the window because it was easier to get up out of.

Pat made two cups of coffee.

She set them on the coffee table.

She did not ask me what was wrong.

I told her.

I told her in the order an adjuster tells the opening narrative of a claim file — date of loss, parties, policy, mechanism, and damage estimate.

I told her the threshold sentence at the kitchen table at six-forty Tuesday.

I told her the surgery at ten-fifteen Tuesday.

I told her the portal disbursement at ten-fifteen on Saturday morning.

I told her the 1992 funeral.

I told her about Vince and Stacey and the Florida condo listings.

Pat listened with her hands folded over the coffee mug.

She did not write anything down.

When I was done she said, “Mar. I have not done a commission complaint in nineteen years. But I will sit with you while you write one.”

She got up and went to the small writing desk in the corner of the living room.

She brought back a yellow legal pad and two black ballpoints.

She set them on the coffee table.

She said, “Start with the policy. Then the cancellation. Then the diversion. Same way we write a property claim.”

I started at the top of the yellow pad.

I wrote: INSURED — Marlene W. Whitfield.

I wrote: POLICY — Long-Term-Care, issued April 14, 2006.

I wrote: PREMIUM — $478/month from BancorpSouth account ending in 4471, paid by INSURED from separate funds, 227 consecutive months.

I wrote: CANCELLATION DATE — initiated October 9, 2025 — five days before scheduled orthopedic surgery of INSURED.

I wrote: NOTICE TO INSURED — none.

I wrote: SIGNATURE ON CANCELLATION FORM — to be obtained from carrier.

I wrote: CASH VALUE DISBURSEMENT — $24,307 ACH to account number not held by INSURED.

I wrote, at the bottom: HARM — coverage gap during post-surgical recovery; financial loss; loss of premium continuity.

Pat read what I had written.

She said, “That is the complaint, Mar. You add the date sequence in the second paragraph and you append the declarations pages and the portal screenshot. Send it to the Mississippi Department of Insurance consumer complaint office in Jackson. Then you call a lawyer.”

I said, “I have a name. Joan Novak gave it to me at the regional retirement gathering in 2024.”

Pat said, “Who.”

I said, “Marsha Pham.”

Pat said, “I have heard of her. She is on Capitol Street.”

I said, “I will call on Monday.”

I sat in the leather chair for another fifteen minutes.

Pat did not make me leave.

She drove me home at twelve thirty-two.

She helped me back inside on the walker.

Gary was still in the garage when I came up the front walk.

I went to the home office.

I sat at the desk.

I did not open the portfolio yet.

I put the yellow pad with the seven complaint lines into the folder marked POLICIES — LTC — 2006 to PRESENT.

I closed the folder.

I closed the door of the office.

I went back to the guest room and lay down on the twin bed.

I slept for an hour and a half.

On Monday morning at nine-oh-eight I called Marsha Pham’s office on East Capitol Street.

Marsha’s paralegal scheduled a consult for Thursday at one in the afternoon.

I spent Monday afternoon at the home office desk pulling the reference documents.

I pulled the original LTC application from April of 2006, signed at the broker office on North State Street.

I pulled the carrier’s annual declarations page for every year from 2007 through 2025 — nineteen pages.

I pulled the BancorpSouth statements showing the four hundred and seventy-eight dollar withdrawal on the second of every month, two hundred and twenty-seven months.

I pulled the power-of-attorney document I had signed for Gary in 2018 for the Pinebelt Capital investment account.

I read the POA at the desk.

I had not read it since 2018.

The POA was a limited durable power of attorney.

It authorized Gary, by name, to manage transactions on the Pinebelt account ending in 9082 — and no other account.

The POA did not authorize transactions on any insurance policy.

The POA did not authorize transactions on the BancorpSouth account ending in 4471.

The POA did not authorize the closing of any account, only the management of trades within the named account.

I filed the POA in the folder marked POLICIES — LTC — 2006 to PRESENT.

I picked up the leather portfolio.

I sat at the desk with the portfolio on my lap.

I unfastened the brass clasp.

I opened the portfolio.

The inside left pocket held the small spiral notebook I had carried for thirty-three years, the one I had used to log mileage to and from every claim site.

The inside right pocket — the one I had not opened in eighteen months because I had not carried the portfolio to a claim site since retirement — held a folded sheet of letter-size paper.

I lifted the sheet out.

I unfolded it.

It was a printout from a real-estate listing service for a unit in a Gulf Coast condominium complex in Destin, Florida — the same complex Vince and Stacey owned in.

The unit was on the fourth floor, two bedrooms, a partial Gulf view.

The list price at the top of the page was three hundred and fifty thousand dollars.

The page had been printed on October 3, 2025 — eleven days before the surgery.

A small handwritten note at the top of the page in Gary’s print said: BUYER — G. Whitfield.

I held the sheet of paper at the corner with my thumb and my index finger.

I read the listing twice.

I did not refold it.

I set it flat on the desk beside the portfolio.

I opened the laptop.

I logged into the Pinebelt Capital account ending in 9082.

The October statement was dated October 1, 2025.

The balance had been forty-seven thousand, nine hundred and fourteen dollars.

On October 6, 2025, a transaction had cleared: WIRE OUT — $11,000 — TO HARTFORD TITLE OF DESTIN — REF: CONDO 4B DEPOSIT.

The wire had been initiated by Gary using the POA authority I had granted him in 2018.

It had been initiated for a real-estate deposit, which was not within the scope of the POA.

The POA had been signed at Pinebelt’s office in front of a broker named Dwight Boudreaux.

Dwight had read the scope aloud to Gary in the same room I had sat in.

I closed the Pinebelt page.

I opened the Florida Department of Business and Professional Regulation portal — the one I had used four times in 2017 to verify out-of-state contractors who had submitted hurricane invoices.

I searched the parcel by the unit number on the printout.

The deed showed: GARY R. WHITFIELD — SOLE TENANT.

The deed showed a recording date of October 24, 2025 — ten days after the surgery.

The deed showed a purchase price of three hundred and fifty thousand dollars, ten percent down at closing, conventional financing for the remainder.

The ten percent — thirty-five thousand dollars — broke out in the closing-cost ledger appended to the deed packet as: $24,307 — LTC POLICY CASH VALUE DISBURSEMENT — and $10,693 — PINEBELT WIRE.

The wire had been eleven thousand on the Pinebelt statement, with three hundred and seven dollars allocated to wire fees and earnest credits.

The closing on the condo had been done on October 24, ten days after my hip surgery, while I was in the guest bedroom on Sweetbriar Lane on the wedge pillow.

Gary had not been at the closing.

He had not flown to Destin.

The closing had been done by power of attorney through Hartford Title of Destin.

The agent on record at Hartford Title was a woman named Reba Munn.

Reba Munn had also been the agent on Vince and Stacey’s closing in 2023.

I sat at the desk for ten minutes after I had logged out of the Florida DBPR portal.

I sat in the dining-room chair my daughter had brought in.

I looked at the leather portfolio.

I looked at the folded printout I had set flat on the desk beside the portfolio.

The portfolio had been on the desk every working day for eighteen months.

Gary had been in and out of the home office on the way to the garage at least three times a week.

I had not opened the inside right pocket of the portfolio in eighteen months.

Gary had been certain I would not.

He had used the portfolio my supervisor Mr. Halverson had given me in 1989 — the one with my own initials in gold leaf — as a quiet storage envelope for the printout of the condo he was buying with the cash value of the policy he had cancelled the morning of my surgery.

He had filed the document of the diversion inside the document of the work that had paid for the policy.

That had been his filing error.

I picked up the printout from the desk.

I picked up the LTC carrier’s cancellation portal screenshot I had printed on Saturday afternoon.

I picked up the Florida DBPR deed printout.

I picked up the Pinebelt wire ledger.

I picked up the POA.

I put all five documents in a single manila folder.

I labeled the folder, in the same red marker the field manuals had used since the 1980s: WHITFIELD — CONDO DIVERSION — OCTOBER 2025.

I put the folder on the desk beside the LTC folder.

I closed the portfolio without putting the printout back inside it.

I refastened the brass clasp.

I put the portfolio back in its place on the corner of the desk.

I went to the kitchen.

Gary was at the breakfast bar with a sandwich.

He said, “Mar. You sleep okay?”

I said, “I slept fine, Gary.”

He said, “I’ll be at Vince’s tonight. Stacey’s making jambalaya.”

I said, “Drive safe.”

He said, “Mar — about the policy —”

I said, “I have an appointment Thursday.”

He said, “What appointment.”

I said, “An adjuster appointment. The way I made them for thirty-three years.”

He did not ask another question.

He took the rest of the sandwich and the keys to the Sequoia and went out through the garage door.

I went back to the home office.

I sat at the desk.

I called Marsha Pham’s office one more time and confirmed Thursday at one.

I closed the door.

The portfolio sat on the corner of the desk where it had sat for eighteen months.

The printout was no longer inside it.

The condo diversion folder was beside it.

Marsha Pham’s office was on the seventh floor of the old Pinnacle Building on East Capitol Street, half a block from the state capitol.

Pat Brewster drove me on the Thursday at twelve-thirty.

I went up on the elevator with the walker.

Marsha’s office was a single corner room with two upholstered chairs across a walnut desk and a window that looked north toward the dome of the capitol.

Marsha was forty-eight years old, in a black sheath dress with a small gold chain, hair pinned back at the nape.

She had practiced elder-law and matrimonial-law work at the same two-name firm for fifteen years.

She had been recommended to me at the regional retirement gathering in 2024 by Joan Novak, who had been the conservation-easement attorney on a Stanislaus County matter for one of my classmates.

I sat in the upholstered chair on the right.

I set the manila folder marked WHITFIELD — CONDO DIVERSION — OCTOBER 2025 on the desk.

I set the folder marked POLICIES — LTC — 2006 to PRESENT beside it.

Marsha asked me to walk her through it from the threshold sentence.

I walked her through it in forty-six minutes.

Marsha did not take notes during the walkthrough.

She wrote in pen on a yellow pad for nineteen minutes after I had finished.

She set the pen down.

She said, “Marlene. The cancellation is reversible under the Mississippi 60-day reinstatement rule. We file the reinstatement request today, on the carrier’s standard form. The carrier owes a reinstatement under the statute unless the policyholder objects, and you are the policyholder. The cash value was disbursed to an account you did not authorize. That goes back.”

She said, “The commission complaint is the lever. The Mississippi Department of Insurance has a consumer-complaint office on West Street. The complaint triggers an internal carrier review within thirty days. The carrier’s loss-prevention department will pull the cancellation form. The signature on the cancellation form will not match yours. We have already established that the POA does not authorize the cancellation. The carrier will void the cancellation and refund the cash value. That is on a six-week track.”

She said, “The diversion is the dissipation case. Eleven thousand wired from the Pinebelt account in breach of the POA scope, twenty-four thousand redirected from a policy held in your name only, both into a condo titled in Gary’s name only — that is intentional dissipation of marital assets in Mississippi. Filed concurrently with the divorce. The settlement will not be fifty-fifty. The dissipation doctrine will swing it. I have run dissipation cases for thirteen years.”

She said, “The retainer is thirty-five hundred.”

I wrote her a check on the BancorpSouth account I had used to pay the premiums for nineteen years.

I signed it Marlene W. Whitfield.

Marsha had me sign three documents at the desk before I left.

The first was the carrier reinstatement request under the Mississippi 60-day rule.

The second was the consumer complaint to the Mississippi Department of Insurance, which she had drafted from the seven lines I had written on Pat Brewster’s yellow pad.

The third was the divorce petition, filed under Mississippi Code 93-5-1, the irreconcilable-differences statute, with a separate count for dissipation of marital assets.

Marsha said, “I am going to file all three on Friday morning. Gary will be served by registered process at the condo in Destin on Tuesday. Until then you do not speak to him about any of this. If he calls you, you put the phone on the table. Anything he wants to say, he says to me. Anything you want to say, you say to me.”

She said, “Are we clear, Marlene.”

I said, “Yes.”

Pat drove me home.

I went back to the guest bedroom and lay down on the twin bed with the right leg on the wedge pillow.

On Friday morning at nine-twenty-two, Marsha filed all three.

On Friday afternoon at four-eleven, my cell phone rang at the home office desk.

The contact on the screen said GARY.

I let it ring.

The voicemail came through at four-fifteen.

I did not listen to it yet.

I had Marsha’s instructions and the voicemail was not the call she had told me to take.

The bank fraud review at Allstate’s regional carrier ran on the second Wednesday after filing.

Marsha came to the house at one in the afternoon with the carrier’s loss-prevention officer on a conference call from Birmingham, Alabama.

The loss-prevention officer was a man named Phillip Drewry.

Phillip read the complaint on the screen in his office in Birmingham.

He read the cancellation form on his second screen.

He said, “Mrs. Whitfield. The signature on the cancellation form is not consistent with the signature on the policy application or the annual premium acknowledgments we have on file. The signature is on a fax we received from a Destin, Florida number we do not have a record of on this policy. We are reversing the cancellation today under the Mississippi 60-day rule. The cash value of twenty-four thousand, three hundred and seven dollars will be restored to the policy by Friday.”

He said, “The disbursed funds will be clawed back via the ACH originating institution. That is a separate eight-week process that may require litigation in Florida. We will refer it to our subrogation department.”

He said, “I am very sorry, Mrs. Whitfield. We will write up a written confirmation today.”

He hung up.

Marsha said, “That is the carrier piece.”

She said, “The commission complaint will run on its own track and may result in a separate enforcement action against the broker who notarized the cancellation. The diversion piece is in front of the court.”

I said, “And Gary?”

Marsha said, “Served Tuesday at nine forty-one in the morning at the condo. He has been calling my office every ninety minutes since.”

I said, “He called me Friday at four-eleven.”

Marsha said, “Don’t pick up. Don’t read the text. The voicemail is content. Save it, do not respond.”

I said, “Understood.”

Marsha left at three.

The temporary-restraining order on the Pinebelt account was granted on the Thursday in the second week of November.

Pinebelt froze the account on receipt at four-twelve in the afternoon.

Gary’s POA was suspended pending divorce settlement.

The Florida title office issued a lis pendens notice on the condo deed.

Hartford Title of Destin had requested a hold on the property pending the Mississippi action.

Reba Munn had not returned my attorney’s calls.

The Pinebelt broker Dwight Boudreaux had confirmed in writing that the October 6 wire had been initiated by Gary, that he had told Gary at the time he was uncertain the wire fell within the POA’s scope, and that Gary had told him on the phone, “Mar signed off.”

I had not signed off.

Dwight had filed the wire under Gary’s signed authorization without contacting me.

Dwight had been suspended for thirty days by Pinebelt’s internal compliance review.

That was the broker’s piece.

On a Tuesday afternoon in the third week of November I was at the home office desk reviewing the carrier’s written confirmation letter and the lis pendens copy when my cell phone chimed with an email notification.

The email was from Stacey Whitfield’s personal Gmail address.

The subject line said: COURTESY — FROM A SISTER-IN-LAW.

The body was three sentences.

It said: “Marlene, I have known about this since August. I should have told you. I am sorry.”

The attachment was a PDF of the original Florida condo purchase contract, dated September 22, 2025 — three weeks before Gary canceled the LTC policy.

The buyer line on the contract said GARY R. WHITFIELD only.

The deposit-source line on the contract said FUNDS TO BE WIRED FROM MISSISSIPPI ACCOUNTS ON OR BEFORE OCTOBER 10, 2025.

That last line — the OR BEFORE OCTOBER 10, 2025 — was the line Marsha said she had been waiting for.

It was the timestamp.

It put the wire-and-cancel sequence on a planned contract.

I forwarded the PDF to Marsha.

Marsha called me back at five-oh-eight.

She said, “Marlene. This moves the case from dissipation to deliberate fraud-on-the-marital-estate. The Mississippi Chancery Court will treat this as an aggravating factor. We will amend the petition Friday.”

She said, “I want a written statement from Stacey if she will give us one.”

I said, “I will call her on Saturday.”

I called Stacey on Saturday morning.

Stacey said yes.

She gave Marsha a sworn statement on the following Tuesday.

She moved out of the condo in Destin on the same Tuesday afternoon, with her three suitcases and her dog Reggie, into a rental in Hattiesburg her sister-in-law owned.

The divorce hearing was scheduled for the second Tuesday in January at Hinds County Chancery Court, Judge Whitney Forrest presiding.

Marsha said the dissipation findings would be presented in open court.

She said the asset division would be calibrated against the contract date and the cancellation date and the closing date.

She said the property settlement, given Stacey’s affidavit, would likely run to sixty percent for me.

She said she would have Gary’s attorney’s response brief by the end of the year.

On the Friday three days after Stacey’s affidavit was filed, Gary called Marsha’s office.

He asked to speak to me through the firm’s conference line.

Marsha put him on the line with her at the desk and me on the line from the home office at home.

Gary said, into the conference line, when I had not said hello: “Marlene. You filed an INSURANCE COMPLAINT? You filed for DIVORCE? Over a CONDO? After 37 years?”

Marsha did not speak.

I did not speak.

Gary said, “Marlene. Look. The condo. We can fix the condo. We can put both names on the title. We can—”

I said, “Marsha has the rest.”

I hung up.

I sat at the desk for two minutes.

I picked up the leather portfolio.

I unfastened the brass clasp.

I looked inside.

The inside right pocket was empty.

I refastened the clasp.

I put the portfolio back on the corner of the desk.

I went to the kitchen.

I made a sandwich.

I ate it standing at the breakfast bar.

The settlement was entered in Hinds County Chancery Court on a Wednesday in the second week of February.

Judge Forrest accepted the dissipation findings as Marsha had presented them.

The asset division gave me sixty percent of the marital estate.

Gary was ordered to refund the twenty-four thousand, three hundred and seven dollars to the LTC carrier directly so the policy could continue uninterrupted from the reinstated October starting point.

He was ordered to refund the eleven thousand dollars to the Pinebelt account.

The Florida condo deed was quitclaimed to joint with right of partition, then ordered sold at market with the proceeds split per the asset division.

The Mississippi Department of Insurance had completed its consumer-complaint review on the second Friday in December and had issued a formal letter of reprimand to the carrier’s broker office for processing a cancellation without verifying the policyholder’s signature.

The reprimand letter had been forwarded to my attorney’s file.

The Pinebelt broker Dwight Boudreaux had completed his thirty-day suspension and had been moved off the senior-accounts desk.

Reba Munn at Hartford Title of Destin had been reported to the Florida Department of Financial Services by Marsha’s office for processing the deed under a contested POA.

I moved out of the house on Sweetbriar Lane on the last Saturday in February.

I packed twenty-one boxes.

I packed my clothes, my mother’s china, the field manuals, the leather portfolio, the folders, the four photographs of my children, the laptop, the dining-room chair, and the lamp from the home office.

I did not pack the casserole dish.

I did not pack the Allstate mug.

I did not pack the Sequoia keychain Gary had given me in 2014.

The movers were a two-man team from a small company off Lakeland Drive that Pat Brewster had used in 2022.

The team took ninety-eight minutes.

They drove the truck six blocks east and four blocks north to the small one-bedroom apartment I had signed a one-year lease on in January.

The apartment was on the second floor of a three-story brick building called the Tinsley.

It had a small kitchen, a living room with two windows facing east, a single bedroom, and a small alcove off the living room with a built-in desk and a window facing the back parking lot of the regional Allstate office on East Capitol Street.

I had chosen the apartment for the walk.

The walk from the front door of the Tinsley to the front door of the regional Allstate office was six blocks and seven minutes.

I had walked it for thirty-three years.

The physical-therapy clinic was nine blocks the other direction, on the second floor of a building on North State Street.

I had two sessions a week through the end of June.

I set up the apartment over the first three days.

I unpacked the kitchen on Saturday.

I unpacked the bedroom on Sunday.

I unpacked the desk and the alcove on Monday.

I set the leather portfolio on the desk under the alcove window at one-fifteen on Monday afternoon, in the same spot, relative to the lamp, that it had sat on the desk on Sweetbriar Lane.

I sat at the desk in the dining-room chair my daughter had loaded into the truck for me.

I unfastened the brass clasp.

I opened the portfolio.

The inside left pocket still held the small spiral notebook from thirty-three years on the road.

The inside right pocket — the pocket Gary had used as his quiet storage envelope — was empty.

I took the new long-term-care declarations page out of the manila folder.

The new page had been issued by the carrier on the first Friday in January when the reinstatement processed.

The new page was dated January 9, 2026.

The owner line said: Marlene W. Whitfield.

The premium payor line said: Marlene W. Whitfield, BancorpSouth account ending 4471.

The premium line said: four hundred and seventy-eight dollars a month.

The cash value line said: twenty-four thousand, three hundred and seven dollars, restored.

The signature line at the bottom said Marlene W. Whitfield in the hand I had signed two thousand and ninety-six claim files in.

I slid the declarations page into the inside right pocket of the portfolio.

I slid the commission-complaint receipt and the reprimand letter from the Mississippi Department of Insurance behind the declarations page.

I slid the divorce-decree acknowledgment behind that.

I closed the portfolio.

I refastened the brass clasp.

I set the portfolio in the spot on the desk under the alcove window.

The leather along the spine had darkened further along the long edge from the eighteen months on the desk on Sweetbriar Lane.

The gold-leaf monogram MW in the lower right corner caught the late-afternoon sun coming through the window.

The portfolio that had carried two thousand and ninety-six claim files for thirty-three years now carried four pages.

It was the only filing that mattered to me at the desk by the alcove window in the apartment on the Tinsley’s second floor.

It was the filing of the thirty-three years of premiums I had paid from a separate account.

It was the filing of the cancellation that had been undone under the Mississippi 60-day rule.

It was the filing of the dissipation that had been corrected by sixty percent on the marital estate.

It was the filing of the new declarations page on which my name was still the owner, the premium payor, and the insured.

The portfolio was eleven and a half inches wide.

The desk under the alcove window was sixteen inches deep.

The portfolio sat to the left of the laptop, with the brass clasp facing the window so that the lower right corner with the monogram was visible from where I sat in the chair.

That was the position the portfolio had been in for thirty-three years on the desks I had used at the regional office and on the desk at Sweetbriar Lane.

It was the position I had chosen for it on the alcove desk on the second floor of the Tinsley.

It would stay there.

On the first Tuesday morning in March, at six-forty-two in the morning, I made grits.

I made them in a small pot on the front burner of the apartment’s stove from the bag of Quaker stone-ground grits I had bought at the Kroger on Lakeland Drive on Sunday afternoon.

I cooked them for twenty-two minutes, the way my mother had cooked them on a stove in our kitchen in 1972.

I added a small pat of butter and a small pinch of salt.

I poured the grits into the small white bowl my daughter had given me for Christmas in 2003.

I carried the bowl to the desk in the alcove.

I set the bowl on the desk beside the leather portfolio.

I sat in the dining-room chair.

I ate the grits with a small spoon from my mother’s china.

I ate them at the desk by the window.

The sun came up over the line of the building across the street.

The sun caught the gold leaf of the monogram on the corner of the portfolio.

I ate the grits in eight minutes.

I drank a glass of water.

While I was finishing the water, my cell phone, which I had left on the desk by the laptop, lit up with a voicemail notification.

The voicemail had come in at six twenty-eight in the morning.

The contact on the screen said GARY.

I picked up the phone.

I tapped the voicemail.

I held the phone to my ear.

Gary’s voice came through.

The recording was forty-one seconds.

It said: “Marlene, we built this for our retirement. We can still do that. The condo can be in both names. Vince is selling out anyway. Stacey is in Hattiesburg now and she’s going to keep talking to people. We can fix this. Mar. Just call me back. We.”

The recording ended.

I held the phone.

I did not play it twice.

I opened the leather portfolio.

I took out the small spiral notebook from the inside left pocket.

I wrote on a fresh page: VOICEMAIL — March 3, 2026 — 6:28 a.m. — GW — content: “We.” — saved, not returned.

I put the notebook back in the inside left pocket.

I refastened the brass clasp.

I set the phone face-down on the desk.

I finished the water.

I rinsed the bowl in the sink.

I set the bowl on the rack to dry.

I picked up my keys from the small wooden tray by the front door of the apartment.

I went down the staircase to the lobby of the Tinsley.

I walked the nine blocks north to the physical-therapy clinic on North State Street.

I checked in at eight thirty-three for a nine o’clock appointment.

The hip surgery had gone well.

The recovery was slow.

The right leg was still weaker than the left.

The therapist, a young man named Curtis, had me walk the parallel bars for thirty-eight minutes that morning.

I walked the bars in the same shoes I had walked two thousand and ninety-six claim sites in.

I walked the nine blocks home at ten thirty-five.

The leather portfolio was on the desk under the alcove window.

The voicemail had not been returned.

The grits bowl was on the rack to dry.

The new declarations page was in the inside right pocket of the portfolio.

My son had called on Sunday from Birmingham.

He had not asked about the divorce.

My daughter had been at the apartment the previous Saturday helping me hang the four photographs on the living-room wall.

She had not asked about the divorce either.

I had not asked them to choose sides.

Thirty-three years of adjusting taught me that the policy is a contract and the cancellation must follow the contract’s terms.

My husband canceled a policy I had paid for nineteen years on the morning of my surgery and called the cash value a household investment.

Households are not policies.

Policies are not households.

The Mississippi insurance code agrees with me.

So does the declarations page in the leather portfolio on the desk under the alcove window at the Tinsley.

The portfolio carries four pages now.

I will add the others as they come.

I will add them on a Tuesday morning, after the grits, in the chair from the dining room, with the brass clasp facing the window.

That is the spot the portfolio is in.

That is the spot it will stay in.