My name is Margaret Huang. I am a licensed forensic accountant — and when the insurance fraud investigation arrived with both our names on it, I had already separated my records from his.

My name is Margaret Huang. I am a licensed forensic accountant — and when the insurance fraud investigation arrived with both our names on it, I had already separated my records from his.

The insurance fraud investigation arrived with both our names on it — and I spent four years as a public adjuster before I met Neil, which meant I knew exactly what to do when I realized the fraud in that letter was his, not mine.

My name is Wanda Ingram. I am a licensed public adjuster. I have spent fifteen years reading insurance claim documentation for discrepancies. The SIU letter named me as a subject. I had four claim files to read. I read them the same way I read every claim. What I found was the same thing I find in other people’s files. The documentation did not hold together.

Every insurance claim tells a story. The documentation either holds that story together or it doesn’t. I have spent fifteen years reading the places where the documentation falls apart—the inflated estimate, the missing contractor invoice, the call log that shows only one person ever spoke to the insurer. I have found these things in other people’s claims for fifteen years.

I was on a call with a Special Investigations Unit investigator for a different insurer regarding a client’s commercial claim the day the letter arrived. I had the client’s damage estimate, the contractor’s invoice, the original adjuster’s report, and the insurer’s initial settlement offer arrayed on my desk.

I walked the investigator through the line items they had disputed, speaking calmly, citing reference numbers. I pointed out the exact page in the adjuster’s report where the square footage measurement was wrong. The investigator listened, verified the page, and adjusted the settlement offer upward by $40,000.

I called my client afterward. “That’s what the documentation does,” I told him. “Not the argument. The documentation.”

The SIU letter regarding my own home arrived in the afternoon mail on a Tuesday. I saw both names on the envelope: Neil J. Ingram and Wanda R. Ingram.

I opened it before Neil got home from work. I read it not as a wife, but as a professional. The letter flagged our homeowners policy for a pattern review. It listed four specific claim numbers over a four-year period.

I recognized the first one—a storm damage claim for the fence. I did not recognize the other three.

I went to the filing cabinet in the den where Neil kept the house documents. Neil handled “house stuff”—that was the term we both used. Repairs, contractors, insurance. I handled the accounts that paid for everything: the premium payments from our joint checking, the mortgage, the household budget. I tracked every outflow. I had never tracked inflow from insurance claims because the claim checks had apparently never gone into the joint account.

I found the accordion folder where Neil kept the physical contractor invoices. He was meticulous about keeping paper records. I pulled the folder out and set it on the table.

Neil came home an hour later. He found the SIU letter open on the kitchen table. He looked at it. Then he looked at me.

“It’s nothing,” he said. His voice was steady. His hands were perfectly still. “Insurance companies overreact to multiple claims. I’ll call the attorney tomorrow.”

He said “nothing” and “overreact” without asking if I was okay. He said it without asking if I had read the claims listed in the letter. He assumed I would defer to his management of the house stuff, just as I always had.

I did not defer. The next morning, I requested the full claim files from the insurer under my rights as a named insured. I received the digital files in three business days.

I sat at my desk at home with the four contractor invoices from Neil’s accordion folder and the four claim documents from the insurer side by side. I compared them.

Claim 1: The fence. Billed to the insurer at $4,200. Contractor invoice in Neil’s file: $1,800.

Claim 2: A water heater replacement, plus “cascading damage.” Claimed at $11,400. Contractor invoice: $3,200 for water heater installation only. No cascading damage repaired.

Claim 3: A deck repair. Claimed at $7,800. Invoice: $3,400.

Claim 4: Window replacement citing “wind damage.” Claimed at $5,600. Invoice: $2,100.

I added up the total overpayment. It was $19,300 across four claims. I have found this amount before in other people’s files. I have always been on the side of finding it, not sitting inside the house that financed it.

I requested the insurer’s call logs for our policy account. Every single call made to the insurer regarding these claims had been made by Neil. My name was nowhere in the communication history.

Neil told himself each claim was essentially deserved. I know this because I understand how policyholders rationalize fraud. The repair to the deck was real, the inconvenience of the water heater was real, and he believed the insurer would absorb a “fair” upward rounding. He had no professional framework for what insurance fraud actually is.

More importantly, he did not understand that I, specifically, would be able to read what he had done in the documentation the way a radiologist reads a scan. He kept it from me not out of profound guilt, but out of a vague sense that I would have “overcomplicated it.” He was right about that. He just did not understand what “overcomplicated” meant when his wife was a licensed adjuster facing federal exposure for his actions.

I had been paying the premiums for the policy from the joint account. I had funded the policy he defrauded. He had deposited the overpayment checks into a separate savings account I found later during the financial discovery of our divorce. This was the arithmetic I had to sit with.

I closed the folders on my desk. I opened them again. I picked up my phone and called Harriet Pruitt, a divorce attorney.

Then I called the SIU investigator directly. I did not tell Neil I was calling. I identified myself by my adjuster license number—I have it memorized—and stated I was calling as the named insured with information relevant to the investigation. I asked for an in-person meeting. The investigator agreed to see me on Thursday.

The SIU investigator’s office was spartan, functional, and intimidating by design. I arrived alone, without an attorney. Neil’s attorney was already there, expecting to represent “the Ingram family.” He was not expecting me to walk in independently.

“Ms. Ingram,” Neil’s attorney said, standing up quickly. “I wasn’t aware you were attending separately. We should discuss your representation situation before we begin this meeting—”

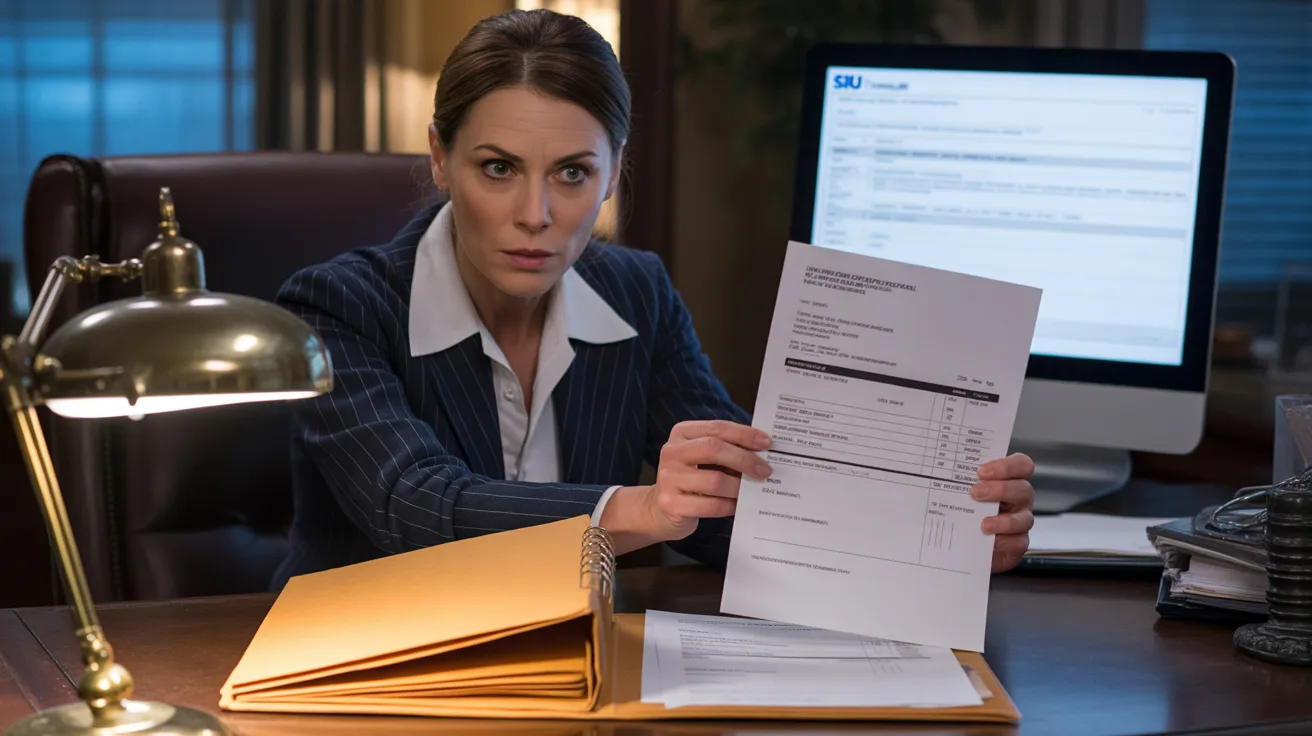

I did not look at him. I opened my briefcase. I pulled out the original contractor invoices from Neil’s accordion folder and placed them on the table, one by one, right in front of the investigator.

“These are the contractor invoices for all four claims listed in the SIU letter,” I said. My voice was the same voice I use when disputing a commercial claim. “I obtained them from our household files. This stack is the claim documentation submitted to the insurer. The submitted amounts and the invoice amounts are different on every single claim. Furthermore, the insurer’s call logs show that Neil Ingram was the sole policyholder contact for all four submissions. My name does not appear in any call record. I have a signed declaration to that effect as well.”

Neil’s attorney stared at the invoices on the table. He swallowed hard. “Perhaps we should take a brief recess.”

The SIU investigator did not take a recess. He looked at the invoices, then looked at me. “Will you leave a copy of these contractor invoices with me, Ms. Ingram?”

“I will,” I said. “I have a second set in my bag.”

I am a licensed public adjuster. I read insurance claim documentation for a living. I have fifteen years of experience identifying the discrepancies between submitted claims and actual contractor invoices. I found them in these four files in the exact same way I find them in client files. The documentation was in front of them. My name was not in any call record. I cleared myself from the fraud investigation in fifteen minutes.

Neil’s attorney called Neil immediately after the meeting. Neil called me. I did not answer. He sent a text: “We need to talk about this.” I did not respond. The next communication he received from me was from Harriet Pruitt.

The SIU closed the investigation against me and referred Neil’s file to the state insurance fraud bureau. The insurer voided the policy and initiated recovery of the overpayments from Neil.

It is four months later. I am in my home office. The house is under an agreement of sale. I am packing one box.

Neil’s fraud referral meant the house equity became part of the asset discovery in the divorce. I did not know how much the fraud had complicated the asset picture until we were deep into the process. I had to hire a second attorney just for the asset portion. I am paying two attorneys from accounts I built alone.

The physical accordion folder that held the contractor invoices is sitting on my desk. I found it in the cabinet when the SIU letter arrived. I didn’t know why he kept hard copies so carefully; I understand now it was simply habit, not calculation. It was the evidence that cleared me.

I place the accordion folder into the box. I keep it. The documentation did its work.

I chose not to fight for the house in the divorce settlement. I have seen enough houses lost to insurance disputes. I did not want to spend more years inside this one than I already had. The equity will be smaller than it should be because of the fraud recovery, but it will be clean.

I am packing one box. I do not know where I am going yet. I have three options for an apartment. I will decide after the box is closed.

Neil handled “house stuff.” He kept the claim files neatly. He always paid the contractor invoices. He just submitted different numbers to the insurer. He managed this for four years because he handled the house and I handled the accounts. He never thought about what it meant that I do what I do for a living. The documentation told me everything. It always does.