I Am The Mortgage Compliance Officer Who Knows How To Pull The Physical IRS Transcripts From The Vault, And The Morning I Checked The W-2s For A Foreclosed Neighborhood, I Understood My Husband Had Been Forging The Federal Underwriting Software—And Let Sixty-Five Families Lose Their Homes To Secure His Corporate Bonus.

I am the mortgage compliance officer who knows how to pull the physical IRS transcripts from the vault, and the morning I checked the W-2s for a foreclosed neighborhood, I understood my husband had been forging the federal underwriting software—and let sixty-five families lose their homes to secure his corporate bonus.

My name is Angela Carter, and for ten years I have been the woman in this bank who knows that a sales manager can type a fake salary into a computer to clear a toxic loan, but the physical IRS transcripts in the vault never lie.

The glow of the dual monitors illuminated the dust motes dancing over my desk. I spent my days inside the Fannie Mae Desktop Underwriter system. It is the gatekeeper of the American dream. The math is absolute. If a borrower’s Debt-to-Income ratio—their DTI—is below forty-three percent, the system approves the mortgage.

If it is higher, the system rejects it. Sales executives see that hard limit as a hurdle. I view it differently. The DTI limit is a mathematical shield. It protects families from financial suicide. A mortgage should be a foundation, not a trap. I tapped the spacebar, waking the second screen.

The printer in the corner hummed, spitting out the final page of a commercial loan application for a massive retail developer. The paper was still warm when I picked it up. It smelled faintly of hot toner and industrial ink. The automated risk software had already greenlit the developer for ten million dollars.

The digital fields were flawless. I ignored the software. I walked out of my cubicle, swiped my badge at the secure file room, and pulled the physical tax returns of the developer’s three shell companies. The digital summary listed zero liabilities. The physical paper told a different story. I traced the employer identification numbers across three state registries, matching the routing numbers line by line.

The developer had a massive, hidden debt structure intentionally obfuscated to bypass the automated checks. The sales director called my desk, demanding the final sign-off to close the quarter. I told him no. I flagged the loan for immediate rejection. I capped my red pen.

I set the heavy file in the outbox. A bank’s software is designed to sell debt, but the compliance officer’s job is to ensure that debt doesn’t become a bomb. I left the rejected file for the director to find.

The ambient clatter of heavy silverware echoed in the upscale bistro across from bank headquarters. The scent of roasted garlic and charred steak hung heavy in the air. Jason sat across from me in a sharp, charcoal wool suit.

His phone buzzed against the marble table every forty seconds, vibrating the water glasses. He was the Regional Sales Manager for Mortgages. We had met at the bank ten years ago in a windowless training room, but while I stayed in the rigid compliance division, he had climbed the cutthroat ladder of corporate sales.

He checked another text, smiling at the screen. He leaned forward, resting his elbows on the marble.

“We’re flooding the zone, Ange. We’re getting people into homes they never thought they could afford.” He picked up his water glass. “The market is hot. We have to capture the volume before the rates change.”

He spoke with the absolute, practiced conviction of a man performing a public service. He wasn’t talking about predatory lending or the mechanics of adjustable-rate debt. He was talking about our future, our success, our next vacation. He reached across the table and covered my hand with his. His palm was warm.

“I’m going to take care of us,” he said.

He paid the check with his corporate card, kissed my cheek, and walked back to the glass tower.

I sat at my desk, reviewing the routine default reports in the quiet of the late afternoon. The digital clock in the bottom right corner of my computer screen read 13:30. It was the exact minute the county sheriff executed the final block of mass eviction orders on the east side of the city.

I looked at the printed foreclosure notice sitting on my keyboard. I uncapped my heavy black ink pen. I wrote 13:30 directly onto the top right corner of the paper. I drew a thick, dark circle around the numbers, pressing hard enough to dent the paper, and set the pen down.

The spreadsheet illuminated the dark office. I scrolled through the default data. The anomaly was massive. Sixty-five mortgages in a single low-income zip code had completely defaulted in the last eighteen months. I checked the origination tags.

All sixty-five were originated by Jason’s division. I pulled the digital files in the Fannie Mae portal. The system showed every single borrower had a massive, six-figure income and perfect DTI ratios at origination.

I dragged my finger across the monitor, matching the borrower profiles to the zip code. Many were listed as fast-food workers, janitorial staff, and retail clerks. The digital portal said they were wealthy. The mass wave of foreclosures said the portal was a catastrophic lie.

The concrete floor of the executive parking garage smelled of exhaust and damp dust. I knelt next to my front tire, holding a digital pressure gauge. Jason’s luxury SUV was parked three spots away.

He was sitting inside with the windows rolled up and the engine running. The acoustic glass was designed to be perfectly soundproof. He didn’t realize his car’s bluetooth system was still synced to the external garage maintenance speaker mounted on the concrete pillar directly above my head.

The speaker crackled. Jason’s voice echoed off the concrete.

“The billion-dollar quota is hit. The Fannie Mae portal cleared every single loan in that zip code.”

Another voice answered. The CEO. “If the CFPB pulls the physical tax transcripts from the vault, they’ll see the massive DTI fraud.”

“I used the executive override,” Jason said. “The digital files are legally locked. Nobody goes down into the paper archives anymore.”

The CEO’s voice dropped. “What about Angela? She’s auditing that sector.”

Jason laughed. A short, dismissive sound. “Angela trusts the digital portal. She trusts me. She’ll never pull the physical IRS paper.”

I did not stand up. I opened my hand. The pressure gauge dropped onto the concrete floor with a sharp clatter. I did not walk to my car. I walked directly to the secure elevator and pressed the button for the subterranean archival vault.

Ten years ago, the induction auditorium at National Bank smelled of new carpet adhesive and catered dark roast coffee. Jason sat next to me in the third row, uncapping a yellow highlighter over his orientation binder. He leaned over, tapping the heavy spine of my compliance manual.

“We’re going to help people build their lives,” he whispered.

The instructor at the front of the room tapped the microphone, calling for quiet. Jason didn’t look at the instructor. He looked at me, his eyes bright and entirely focused. He wasn’t looking at the corporate slides.

He was looking at his future. I closed my manual. I believed he wanted to do banking the right way. We signed our employment contracts at the exact same time, handing the pens back to the proctor.

Two years ago, the bank merged with a coastal conglomerate. The regional sales quotas quadrupled overnight. Jason stood in our kitchen at midnight, the harsh blue light of his laptop reflecting off the dark granite island.

“A billion dollars, Ange,” he said. He scrolled rapidly through the new executive compensation tiers. “If my region hits a billion in originated volume, the bonus is two million.”

He picked up a crystal decanter and poured a measure of scotch. He did not offer me a glass. He stared at the glowing numbers on the screen. He didn’t speak again for twenty minutes. He just kept scrolling, calculating the sheer volume of debt required. He closed the laptop at three in the morning. He left the empty glass on the counter.

Eighteen months ago, I laid the quarterly risk assessment report directly on the center of his desk. His corner office smelled of expensive leather upholstery and sharp citrus cologne.

“You are targeting the 90220 zip code with high-risk adjustable-rate products,” I said. “Those are low-income borrowers. They cannot survive a standard rate hike.”

Jason did not look at the printed report. He reached up and adjusted the knot of his silver tie.

“The market will absorb the risk,” he said. His voice was completely flat. “I am executing the CEO’s directive. We provide the liquidity.”

He picked up the risk assessment with two fingers. He slid it off his desk and dropped it into the secure shredding bin. He picked up his golf clubs and walked out of the office.

Yesterday, the sky was a flat, bruised purple over the east side of the city. I parked my car on 4th Street. Moving trucks lined both sides of the curb. The Martinez family—a household I had seen flagged in the default files—were carrying a twin mattress down their concrete front steps.

Two young children sat on a plastic cooler on the sidewalk. Two county sheriffs stood on the porch. One held a clipboard. The other held a drill, bolting a heavy sheet of plywood over the front door.

The physical reality of Jason’s digital volume was an entire neighborhood being systematically erased. I watched Mr. Martinez hand his house keys to the deputy. I turned around and walked back to my car.

I had stopped Mr. Martinez on the sidewalk before I drove away. I asked him how the bank had ever approved his original application. He set down a cardboard box. He pulled a folded, sweat-stained paystub from his wallet.

He made thirty-five thousand dollars a year as a warehouse worker. The Fannie Mae portal claimed he made one hundred and twenty thousand. The physical paper in his calloused hand violently contradicted the massive digital profile on my monitors.

Back at my desk, I pulled the backend access metadata for the Martinez loan. The massive digital income wasn’t verified by the underwriting department. The system logged a manual override.

The credential used to bypass the income verification lock was a “Sales Executive Override.” The identification number belonged to Jason. He hadn’t just bent a lending rule. He had manually typed fabricated, massive salaries for all sixty-five families into the federal clearing system.

I needed the physical proof of the motive. The corporate directive. That evening, Jason was at a golf dinner with the CEO. I knelt on the hardwood floor of his home office, looking for a small earring I had dropped. I swept my hand under the heavy steel of his locked filing cabinet.

My knuckles brushed against something hard. It wasn’t an earring. It was a small, black magnetic spare key box, stuck to the underside of the bottom drawer. I pulled it free. The box was perfectly concealed, a physical dead drop in his own home.

I popped the plastic lid. Inside was a printed, highly confidential email from the Bank CEO. “Jason, your region must hit one billion in originated volume by the end of Q3 or your division is restructured. Clear the paper. Do whatever it takes to fund the loans. Your two-million-dollar bonus depends on it.” I folded the paper along its original crease.

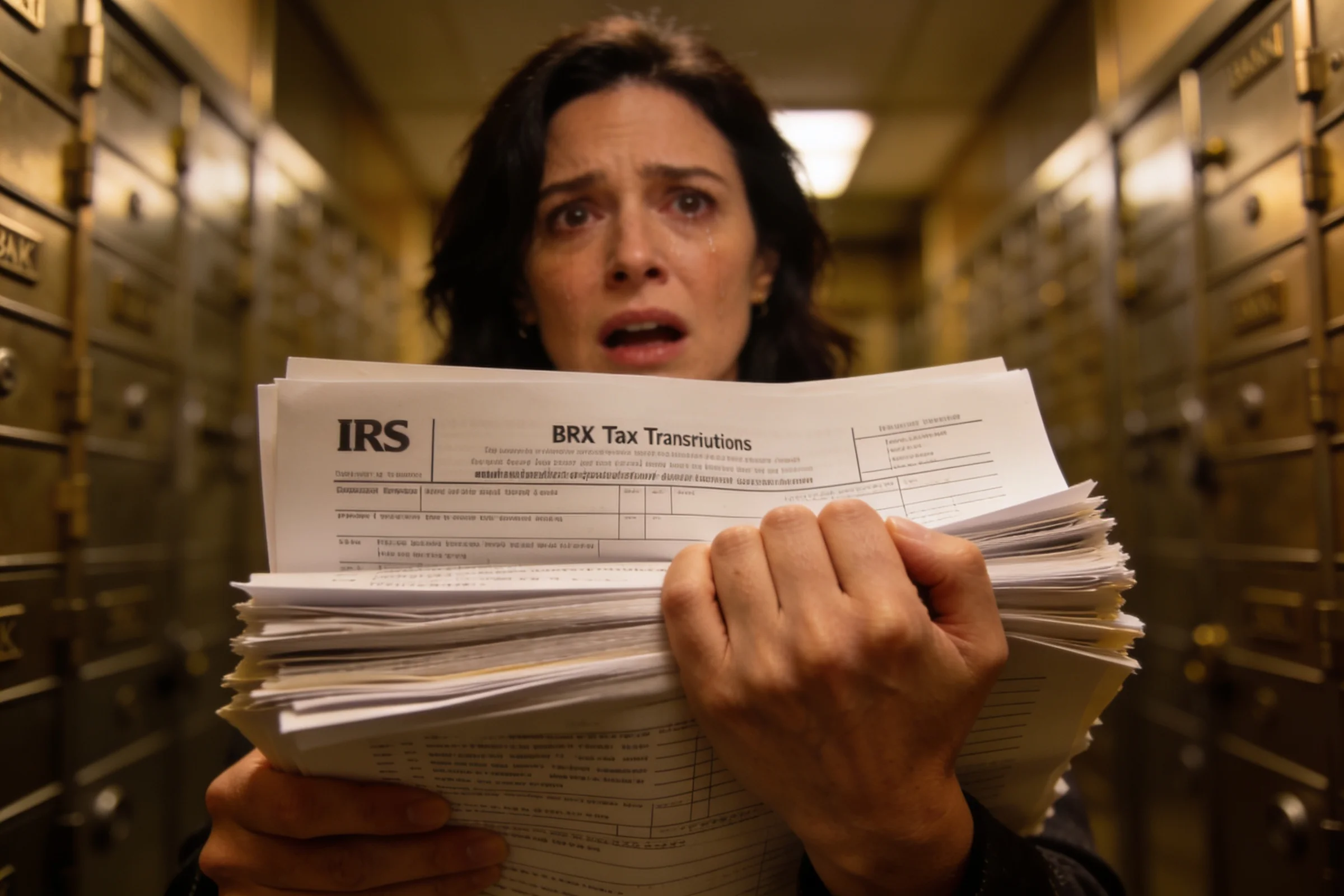

The next morning, I bypassed the IT department entirely. I took the secure elevator down to the bank’s subterranean archival vault. The air down here was cold. It smelled of aged paper and dry dust. I swiped my senior compliance badge.

The heavy steel door unlocked with a deep mechanical clack. I walked down aisle four. I pulled the master boxes containing the original, paper loan closing folders for the sixty-five foreclosed families. I opened the Martinez file.

Inside was the legally verified IRS W-2 tax transcript filed at closing. The physical tax document proved he earned exactly thirty-five thousand dollars. Jason hadn’t just inflated numbers. He had actively orchestrated massive federal wire fraud.

I sat in my car parked in our driveway. The hidden CEO email and the heavy stack of physical IRS W-2 transcripts sat on the passenger seat. I looked at the printed foreclosure notice. The timestamp was there. 13:30.

At exactly 13:30, sixty-five families had their lives shattered because the man I married wanted a two-million-dollar bonus. 13:30 wasn’t just a time. It was the exact minute an executive’s greed had manifested into absolute, physical violence against a neighborhood. The numbers felt like a permanent stain. I uncapped my yellow highlighter. I pressed the neon tip onto the paper. I highlighted the 13:30 timestamp. I picked up a heavy-duty stapler from my bag.

I stapled the physical IRS transcripts directly to the hidden CEO email. I placed them both into a heavy blue federal reporting folder. I got out of the car. I opened the trunk. I placed the folder inside and locked the trunk.

I got back into the driver’s seat. I did not drive to the bank’s internal compliance board. The CEO was complicit. I turned the key in the ignition. I put the car in drive and drove directly to the local field office of the Consumer Financial Protection Bureau.

The overhead pendants cast sharp circles of light onto the dark marble island in our kitchen. Jason stood by the sink, holding a heavy crystal wine glass by the stem. He poured a deep red Cabernet, the liquid catching the light and swirling against the glass.

He set the heavy bottle down on the stone. He was wearing a fresh white shirt, the collar unbuttoned, his silk tie loosened and draped over a stool. He was expansive. Triumphant. On Friday, the CEO was standing at a podium at the National Banking Summit to formally announce Jason’s promotion to National Director of Sales.

Jason took a slow sip of the wine. He looked at the reflection of our kitchen in the dark windowpanes.

“They finally approved the budget for the archive cleanout,” he said. His tone was casual, conversational. “We’re initiating a legacy paper digitization and shredding protocol for the subterranean vault. We are going completely paperless to save on storage costs. The vendor starts Thursday afternoon. Everything older than twelve months gets destroyed.”

I stood on the opposite side of the island. My hands rested flat on the cool marble. Thursday afternoon was tomorrow. He was going to shred the physical IRS transcripts before the CFPB could secure a federal warrant. He was closing the final loop.

“The market shifts, Ange,” he said, turning back to look at me. “It was an unfortunate market correction. That’s all.”

I did not move. I watched his hands.

“The borrowers knew the risks when they signed the paper,” Jason continued. He walked around the island, standing close enough that I could smell the sharp oak of the expensive wine. “We provided liquidity to the system. The bank made massive profits, and we’re secure for the rest of our lives.”

He completely insulated himself from the shattered families. He hid behind the fake digital incomes he had typed into his computer. He viewed himself as a financial visionary.

“We can finally start looking at that summer house in the Cape,” he said. He reached out and tapped the rim of his glass against the marble counter. It made a sharp, high-pitched ring. He walked out of the kitchen, taking the glass with him. He left a small, dark circle of wine on the white stone.

The fluorescent lights in the bank’s subterranean vault buzzed with a low, irregular hum on Thursday morning. The air down here was artificially dry, smelling of aged cardboard, binding glue, and dust.

Chloe Martins, the vault archivist, was pushing a large grey plastic bin down the center of aisle four. The side of the bin was stamped with the bright red logo of a commercial shredding vendor.

I stepped into the aisle. My heels clicked loudly against the polished concrete. The heavy steel fire door locked shut behind me with a loud mechanical clack.

Chloe stopped the bin. “They want the 2024 boxes cleared and fed into the trucks by two o’clock,” she said. She wiped paper dust off her hands onto her slacks. “Are you pulling a file before it goes?”

I held up my senior compliance badge. The thick plastic caught the harsh overhead light.

“I need to conduct a blind audit of the 90220 zip code origination files,” I said. “I have to sequester the physical boxes before the vendor arrives. Clear the aisle, Chloe.”

Chloe looked at the badge. She looked at the massive stack of cardboard archive boxes on the steel shelving unit. She did not argue with a senior compliance officer. She nodded, grabbed the handles of the grey bin, and pulled it backward out of the aisle. I listened to the wheels squeak against the floor until the secondary security door opened and latched shut.

I walked to the steel shelving unit. I grabbed the handle of the first master box. It was heavy. It contained the physical, legally verified IRS W-2 transcripts for the Martinez family and twenty others. I pulled it off the shelf, the cardboard scraping loudly against the metal. I set it onto a metal rolling cart. I went back for the second box. I pulled it down. Then the third.

I loaded the physical records of sixty-five foreclosed families onto the cart. I did not scan the barcodes. I did not enter my ID into the digital tracking system. I bypassed the network entirely. I committed an overt act of theft against my own bank, physically stealing corporate archives.

I had built a life with Jason Carter for ten years. I had believed him when he said we were helping people build their lives. There were exactly eighteen months between the day he bypassed that income lock and the minute the sheriff executed the evictions at 13:30.

Eighteen months where I trusted the man I loved instead of auditing the paper in the vault. That is not compliance. That is complicity in the destruction of a community. I loaded the physical tax transcripts into my car so his digital lie could never be shredded.

The wheels of the metal cart rattled loudly over the uneven concrete of the bank’s subterranean loading dock. The morning air outside was bright and humid, loud with the sound of delivery trucks idling. I unlocked my car. I lifted the first heavy cardboard archive box off the metal cart and shoved it deep into my trunk.

The cardboard caught and dragged against the carpet. I lifted the second box, pushing it in flush against the heavy blue federal reporting folder that held Jason’s hidden email. I loaded the final box. I slammed the trunk shut with both hands. I left the empty metal cart sitting sideways on the concrete ramp.

I got into the driver’s seat. I did not drive back up to the compliance division. I did not check my email. I put the car in gear and drove out of the city center, heading directly toward the massive glass domes of the convention center.

The parking lot was entirely full of luxury vehicles. The National Banking Summit was already underway. The atmosphere was highly corporate, buzzing with the sound of thousands of executives networking. I parked in a loading zone near the service entrance.

I walked around to the trunk. I popped the latch. I pulled out one of the heavy cardboard archive boxes. I placed the blue federal folder flat on top of it. I slid my hands under the bottom of the box and lifted. The weight of the raw paper pressed hard against my ribs. I turned around. I walked up the wide concrete steps. I pushed through the massive glass doors of the convention hall.

The National Banking Summit was held in the Grand Pavilion of the downtown convention center. The vaulted glass ceiling filtered the morning sun, casting long, sharp shadows across the polished granite floors of the lobby.

The air smelled of expensive espresso and crisp, new lanyards. Thousands of banking executives, financial journalists, and federal regulators milled around the registration tables. The digital signage above the main doors flashed the logo of the National Bank in continuous, high-definition loops. The atmosphere was dense with corporate wealth and aggressive optimism.

I bypassed the main registration line. I did not wear a name badge. I carried the heavy cardboard archive box with both hands, the thick blue federal folder resting flat on top of the corrugated lid. The weight of the raw paper pulled at my shoulders.

The muscles in my forearms burned. I walked past the security checkpoint, flashing my senior compliance identification. The guards did not stop a bank officer carrying a box of files.

I pushed through the heavy acoustic doors at the back of the main hall.

The sheer scale of the room was overwhelming. Three thousand chairs were arranged in perfect, sweeping arcs, all facing a massive, raised stage. The carpet was thick enough to absorb the sound of my footsteps. Three towering LED screens projected a live feed of the podium.

Frank Dolan, the Chief Executive Officer of the National Bank, stood behind the microphone. He wore a bespoke navy suit. He held a crystal award geometric and sharp in the stage lights.

“The modern mortgage market requires aggressive innovation,” Dolan’s voice boomed through the line-array speakers, echoing off the back walls. “It requires leadership that understands how to streamline the pipeline without compromising the integrity of the institution.

Today, we recognize a man who has done exactly that. He has driven our originated volume past the one-billion-dollar mark, setting a new standard for this bank and this industry. Please welcome your new National Director of Sales, Jason Carter.”

The applause was a physical force. Three thousand executives clapped in unison. The sound washed over the room in a massive, rolling wave.

Jason walked onto the stage from the right wing. He looked immaculate. His posture was perfectly straight. He smiled a practiced, confident smile, waving briefly to the front rows. He shook the CEO’s hand and accepted the heavy crystal award.

He stepped up to the podium and adjusted the microphone. The applause slowly died down, replaced by the hushed, expectant silence of a captive audience.

Jason looked out over the sea of faces.

“We have revolutionized the mortgage pipeline,” Jason said, his voice smooth and resonant through the massive speakers. “Our streamlined underwriting proves that massive volume and robust compliance can coexist.”

He did not get to say another word.

The heavy acoustic doors at the back of the hall swung open, slamming hard against the rubber wall stops. The sound was like a gunshot in the quiet room.

Agent Marcus Hayes walked into the convention hall. He did not wear a tailored suit. He wore a dark federal windbreaker. Four armed United States Marshals and six FBI agents walked in behind him. They spread out immediately, moving in a practiced, tactical formation to block the exits.

The silence that fell over the convention hall was absolute. It did not happen all at once. It rippled forward from the back rows to the front as three thousand banking executives turned their heads to look at the federal agents. The air in the room suddenly felt heavy and still.

Agent Hayes walked straight down the center aisle. He did not rush. He did not look at the crowd. He looked directly at the stage. The only sound in the massive room was the heavy, rhythmic thud of federal boots on the carpet.

Dolan stepped back from the podium. His hands dropped to his sides. Jason stood completely still.

Agent Hayes reached the front row. He walked up the short flight of stairs on the side of the stage. He approached the CEO. He reached into his jacket and produced a folded white document. He handed it to Dolan.

“Frank Dolan,” Hayes said. His voice was not amplified, but in the dead silence of the hall, the front rows heard him clearly. “I am serving a federal criminal warrant from the Consumer Financial Protection Bureau. Effective immediately, the United States government is placing a total freeze on the National Bank’s entire mortgage lending charter. Your operations are halted.”

Jason leaned into the microphone.

“The CFPB has no jurisdiction over automated underwriting,” Jason said. The speakers amplified his voice, making it sound hollow and defensive. “The Fannie Mae portal legally cleared every single loan in our portfolio.”

I walked out from the shadows at the back of the hall.

I carried the heavy box down the center aisle. I did not look at the thousands of executives staring at me. I kept my eyes on the stage. The cardboard scraped against the fabric of my jacket. My breathing was slow and measured. I reached the front row. I walked up the side stairs. I stepped onto the stage.

I walked to the podium. I placed the heavy cardboard archive box directly on the edge of the stage, right next to Jason’s crystal award.

The box hit the floor with a dull, heavy thud.

Jason looked at the barcode on the side of the box. He recognized the vault index number. He looked at the blue federal folder resting on top. He looked at me.

“You brought stolen vault archives into a national summit?” Jason said. His voice was low, strained, bleeding out over the microphone. “You’re destroying our lives, Angela. You’re throwing away everything we built.”

I did not raise my voice. I did not look away.

“You didn’t make us rich,” I said, speaking clearly into the silence. “You forged federal underwriting software and orchestrated the destruction of sixty-five families to secure your two-million-dollar bonus.”

I opened the blue folder. I pulled out the top sheet.

“The Fannie Mae income fields were manually overwritten by your executive override credential,” I said. I placed the page on the podium. “The physical IRS tax transcripts in this box prove those families were making minimum wage. The loans were mathematically toxic the second you funded them.”

I pulled out the second sheet. The printed email. I set it down next to the transcripts.

“The secret email you hid under your filing cabinet proves you knowingly crashed an entire neighborhood just to hit your billion-dollar volume target. You destroyed generations of wealth so you could buy a summer house, and you broke federal banking law to do it.”

Frank Dolan had been holding the federal warrant in his right hand. He looked down at the physical IRS W-2 transcripts on the podium. He saw the printed email with his own letterhead and his own signature block demanding the billion-dollar quota.

His face went completely pale. The blood drained from his cheeks. He dropped the warrant onto the stage. He stepped completely away from Jason, backing up until he hit the rear curtain. He frantically raised his hand, signaling the bank’s massive corporate legal team in the front row to instantly draft a statement disavowing the Sales Manager.

A senior Federal Reserve Regulator had been sitting in the very center of the front row. He had his legs crossed, listening politely to the keynote just three minutes ago. He saw the CEO retreat. He saw the federal freeze. He physically stood up, dropping his event program onto the floor.

He pulled his mobile phone from his jacket pocket and dialed a number, turning his back to the stage to instantly initiate a catastrophic, multi-billion-dollar federal audit of the bank’s entire national portfolio.

Agent Marcus Hayes had been standing procedurally near the stairs, watching the exchange. He looked at the physical evidence on the podium. He stepped directly onto the center of the stage. He reached behind the podium and unplugged Jason’s microphone. The small green light on the console died. Hayes nodded to the two federal marshals waiting at the bottom of the steps.

Jason looked at the heavy cardboard box of physical IRS transcripts. He looked at the dead microphone. He looked at me, the woman who enforces the rules. He adjusted the lapels of his expensive suit.

“I hit the billion-dollar quota,” Jason said, his unamplified voice small and empty in the cavernous room. “I made us rich.”

The marshals grabbed his arms. They pulled his hands behind his back. The steel handcuffs clicked loudly, locking around his wrists. They turned him around and marched him off the stage, walking him back up the long center aisle, his banking empire and his marriage completely shattered in front of the world.

The streetlights flickered on along 4th Street, casting long, pale shadows across the cracked sidewalks. The evening air smelled of cold asphalt and dry, overgrown lawn grass. There were no cars parked in the driveways. There were no lights on in the living rooms. A plastic tricycle lay abandoned on its side near a storm drain.

Jason was sitting in a federal holding cell wearing a standard-issue jumpsuit. His two-million-dollar bonus had been seized by the Department of Justice. The National Bank CEO had surrendered his passport to a federal judge, and the entire predatory lending division had been padlocked by federal marshals. The toxic loans were halted.

But the Martinez family was still sleeping on an air mattress in a cramped, rented room across the city. The sixty-four other families were scattered, their credit destroyed, their equity erased. A federal court would eventually establish a victim restitution fund, and in three or four years, the families might receive a partial settlement check. But a federal check does not un-bolt a front door.

A check does not rebuild a neighborhood that was surgically dismantled for corporate volume. The corruption was rooted out, but the absolute destruction inflicted on this street was permanent. The houses sat empty, held indefinitely in federal receivership, their windows dark behind heavy sheets of oriented strand board.

I sat in the driver’s seat of my car, parked along the curb. The engine was running, the low hum vibrating through the steering wheel. The dashboard cast a pale blue light across my hands. I watched the digital clock in the center console. The numbers glowed sharply in the dark cabin. 13:28.

The street outside was completely silent, stripped of the families who had built it. 13:29. I kept my hands on the wheel. I stared at the numbers. The clock flipped to 13:30. Yesterday, this exact minute was the mechanical execution of a mass eviction.

It was the precise moment the sheriff’s drill had secured the final sheet of plywood over a family’s life. The blue numbers remained steady. Nothing happened. The street stayed quiet. The numbers flipped to 13:31. The time was just a mundane part of the afternoon again. It held no hidden executive overrides. It triggered no mass evictions. The machinery of the theft had been broken. I reached forward and turned the key. The engine died.

I opened the car door and stepped out. The wind rustled through the dry branches of an oak tree in the nearest yard. I didn’t look at my phone. I didn’t open the banking software on my laptop.

I walked around to the back of the car and opened the trunk. I reached past the empty space where the heavy cardboard archive boxes had been. I pulled out a heavy, forged steel crowbar. The metal was heavy and cold against my palm.

I walked across the dead grass. I climbed the three concrete steps of the Martinez house. I stood on the porch, looking at the heavy plywood bolted over the doorframe.

A corrupt sales manager can type a fake salary into a digital portal to make a toxic loan look compliant if he only cares about his bonus. But the IRS doesn’t care about banking quotas or executive overrides. They only record the exact physical taxes a person paid, and eventually, the paper transcripts in the vault tell the truth.

I lifted the crowbar. I wedged the flat, forged edge deep under the side of the heavy plywood. I planted my boots on the concrete porch. I gripped the steel with both hands and leaned my weight back. The galvanized screws groaned against the wood frame. I pushed harder, and the board began to splinter.