My husband’s sons offered to help me through the estate transition — and 93 days later I found a $280,000 transfer from his accounts to an account I’d never seen, and a will amendment I’d never seen, and a probate petition listing them as co-executors.

My husband’s sons offered to help me through the estate transition — and 93 days later I found a $280,000 transfer from his accounts to an account I’d never seen, and a will amendment I’d never seen, and a probate petition listing them as co-executors.

My name is Beverly Cross. I am a forensic bookkeeper. I have managed accounts for twenty-two years, including my husband’s business accounts for eighteen of those years. I print month-end statements. Paper doesn’t change retroactively. Screens do. I have the statement from twelve days after Roland died. The transfer is on it.

I was reviewing a restaurant client’s accounts when the discipline of my profession saved me from the deception of my family. I was tracking a cash flow irregularity across three months. It took me eleven minutes to identify the source: a vendor’s payment terms had shifted from net-30 to net-15, and the client hadn’t adjusted their payment schedule to match the new terms.

I called the client and explained it simply. “You’re paying on time for a contract that’s no longer on net-30. Fix the schedule and you’ll recover the float by Q4.”

The client paused. “How did you find that? I’ve been staring at the software dashboard for a week.”

“I print statements every month and I compare them,” I said.

I print month-end account statements for every account I manage. Roland’s business accounts were included in that routine. It is not an issue of efficiency; it is the fundamental way I work. The digital record is fluid. It can be overwritten, amended, and updated by someone with administrative privileges. The printed page is absolute. Paper doesn’t change retroactively. Screens do.

Roland ran a small commercial cleaning company. He built it from two vans to a fleet of fourteen. For eighteen years, I managed the books. I handled the payroll, the accounts payable, and the quarterly tax filings. Ian and Troy, his adult sons from his first marriage, had never been involved in the business. They lived in different states for most of Roland’s life, working in different careers. They were present in the way adult children from first marriages are present: at holidays, at Roland’s birthday dinners, at events that required their inclusion. They were polite to me. They called me “Bev.” I always thought they did not like being required to call me anything at all.

When Roland died, they offered to help with the estate transition. It was the first time either of them had asked about the business in eighteen years.

I agreed to give them 90-day access to the business accounts because a probate attorney—one they had found, one I had not met—told me it would help expedite the estate settlement. I was grieving. I was managing the estate documents, the death certificate filings, the life insurance claims, and my own dozen bookkeeping clients all at once. I was operating under the assumption that Roland’s sons, whatever their other qualities, would not steal from their father’s widow. This is the assumption I am still accounting for.

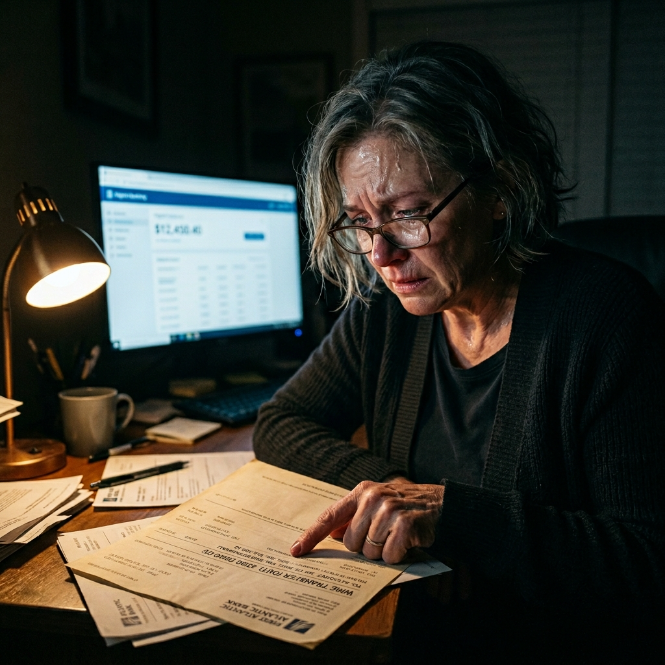

Ninety-three days after Roland’s death, I was doing my monthly statement review. Not for the estate, just habit. I pulled Roland’s business account statements. I was not looking for anything in particular. I found it because I always print. I found it because paper doesn’t change.

The current balance in Roland’s business account was $280,000 lower than the last statement I had printed. I looked at the transfer date: twelve days after Roland died. I looked at the destination: an account routing number I did not recognize.

Ian called me later that same day. He called before I had said a word to anyone. The timing told me he was watching the accounts, monitoring my login activity.

“Beverly,” he said, his voice easy and informational. “Troy and I have been managing some estate-related transfers for the business — moving assets into a holding account for the probate process. It’s standard estate management. We’ll walk you through everything at the family meeting next week.”

He used “estate management” and “standard” in the same sentence. He spoke with the confidence of someone who has never met a forensic bookkeeper.

I compiled my printed statements for the past eighteen months. I laid them out on my desk. The $280,000 transfer appeared on exactly one statement—the one post-dating Roland’s death, post-dating my grant of access to the boys. They had made the transfer on day twelve. Not at the end of the 90-day window, but near the very beginning. They were not careful. They believed my grief was enough to obscure what they did.

I opened my filing cabinet and pulled my copy of Roland’s original will. Roland signed it six years ago. I was in the room when he signed it; I witnessed it. I have a physical copy with the wet ink signatures.

I went online and searched the county probate court docket for Roland’s estate. I found the petition Ian and Troy had filed. Attached to it was a will amendment, dated two years ago, naming Ian and Troy as co-executors of the estate with equal authority to myself.

I looked at the amendment document on the screen. It bore Roland’s signature, or an approximation of it, and was signed before a notary named Dale Pryor.

Forensic bookkeeping is the science of establishing what is real. I searched the state’s notary commission records for Dale Pryor. The state had no registered commissions under that name for that year.

I sat at my desk with the printed bank statement in front of me. The transfer amount. The date. Twelve days. I have been a bookkeeper for twenty-two years. I know exactly what a fraudulent transfer looks like. I have found them before in client accounts. I have traced them through shell corporations and dummy vendor invoices. I had never found one in my own accounts.

I sat with this reality for a long time. The quiet of the house pressed against the windows. Then I picked up the original will, the printed statements, and the probate docket printout.

I called Patricia Crane.

Ian told himself this was fair. I know this because I know how fraud is rationalized. He told himself that I would be provided for by the life insurance and the house, and that the business was essentially the inheritance of Roland’s sons from his first family. He told himself that a second wife of twenty-two years had “received enough.” He managed to believe this because he had never examined the arithmetic of what “enough” meant in this family for those twenty-two years. Troy followed Ian because he always has. Ian proposed, Troy agreed, and they built a plan that required forgery to execute.

I met Patricia Crane at her office the next morning. I gave her the printed statements and the original will. I also gave her a handwritten timeline of everything that happened from Roland’s death to day 93. Forensic bookkeepers make timelines.

Patricia filed three documents the following week: a probate fraud complaint challenging the will amendment as fabricated, a civil theft complaint for the $280,000 transfer, and an emergency petition to remove the step-sons as co-executors, citing the fraud.

She also contacted the man named Dale Pryor—not a notary, but a former coworker of Troy’s who had briefly held a notary commission in a different state five years prior. Patricia obtained a written, sworn statement from him.

The co-executor petition hearing was held in probate court eleven months after Roland died. The courtroom was paneled in dark wood, smelling of dust and old paper. Ian and Troy sat at the respondent’s table with their attorney. Patricia and I sat at the petitioner’s table.

Ian’s attorney stood up to present the amendment. He was a man who relied heavily on the presumption of family goodwill. “Your Honor, the will amendment represents Mr. Mercer’s final wishes regarding his estate and the equitable distribution of his business interests among his children.”

Patricia Crane stood up. She did not argue intent. She argued facts.

“Your Honor, the amendment in question lists notarization by a Dale Pryor on March 14, 2024. The state notary commission has no record of Dale Pryor holding a commission in this state on that date. We have submitted Exhibit B, a sworn written statement from Mr. Pryor stating explicitly: ‘I did not notarize this document.'”

Ian looked at Troy. It was a sharp, sudden movement. Troy looked back. Neither of them spoke, but they went entirely still at the exact same moment. I watched this happen.

Patricia continued. “Furthermore, we have submitted Exhibit C, printed account statements demonstrating that twelve days after the deceased’s passing, the respondents utilized their temporary access to transfer $280,000 from the business accounts to a private holding account under their exclusive control.”

The judge looked over the bench at Ian. “Is this accurate, Counsel?”

Ian’s attorney looked at the documents Patricia had submitted. He had not seen the printed statements. He had only seen the digital records Ian had provided him.

I stood up.

“I print account statements every month,” I said. My voice was steady. It echoed slightly in the high-ceilinged room. “It is not efficiency—it is how I work. Paper doesn’t change retroactively. The statement from twelve days after my husband died shows $280,000 leaving an account his sons had been given 90-day access to. The original will is dated six years ago. I have a copy. I was in the room when he signed it.”

The probate judge called a recess pending a formal review of the notarization discrepancy. Ian and Troy walked out with their attorney. Ian’s pace was significantly slower than it had been when he arrived. He did not look at me as he passed our table. Troy did. He looked at me once, right at the door. It was a look I could not read, and I did not try to. I turned back to Patricia Crane and asked what the timeline was for the emergency executor removal petition.

The step-sons were removed as executors. The $280,000 transfer was recovered through civil judgment. The estate was settled according to the original will.

It is now eleven months and two weeks since Roland died. The case file is closed.

I am sitting at the kitchen table. My desk is clear. I am not printing statements this week. I gave myself a week off. I have not taken a week off in fourteen years.

I sat at a probate hearing and formally accused Roland’s sons of forging his will. I did it because it was true, and because I am a forensic bookkeeper, and the evidence was absolute. The printed statement from day twelve is in the legal file now, no longer on my desk. It was the thing that saved the estate, and now it is an absence on my cleared desk during the one week I am not working.

I would do it again. I do not know if Roland would have wanted me to. I think he would. He valued precision, and he valued the business we built together. But I do not know with certainty. I never asked him if he knew what his sons were capable of. He never mentioned it. I am left with the arithmetic of their actions, not his intentions.

Ian told me it was standard estate management. He transferred $280,000 to an account I’d never seen, and I found it because I was doing what I always do. It took me eleven minutes to find an irregularity for my restaurant client the week before. It took me eleven months to close this one. The difference was Roland.

It is day three of my week off. I am sitting in Roland’s chair at the kitchen table. The house is very quiet. I am finding out what I do with quiet.